Answer: $19,800

Explanation:

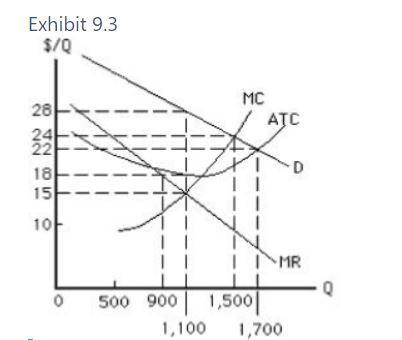

The Monopolist will produce at a quantity where Marginal Revenue equals Marginal cost.

From the exhibit, that quantity is shown to be 1,100.

At that quantity, the average total cost incurred is $18.

Total Cost

= Average total cost * quantity

= 18 * 1,100

= $19,800

Answer:

The overview of that same problem is defined throughout the explanation segment below.

Explanation:

- My understanding would be that privately owned businesses will happily inform anyone who queries.

- Publicly traded companies are identified by the mark as well as the worker's everyone seems to be testing their price of the stock-to decide according to one's interest in share capital.

But things are going to change, the FED had already lost together with all remaining remains of knowledge that convince one where the worth of someone's inventory since they have lost Market Exploration.

I feel like this is a trick question because it would not be that simple of a decision but if those were the only two things to consider then I guess it would be true. But in real life you would have to worry about employment costs, advertisement of the new store, who will manage each store when you are at the other store, etc. There would be so many more things going into that decision than just 450,000-400,000=50,000. But I would go with true.

Hope that helps.

Answer:

B

Explanation:

(c) Any person who engages in the business of money transmission without a license as provided herein shall be guilty of a felony and, on conviction thereof, shall be fined not more than $25,000, or imprisoned for not more than 5 years, or both. (July 18, 2000, D.C. Law 13-140, § 24, 47 DCR 3431.) § 26–1024. Promulgation of rules.

I hope this helped.