Answer:

I think the answer to your question is true(not sure sha)

Answer:

a. realized location economies.

Explanation:

The realized location economics refers to the economics in which the companies go throughout the globe to determine and operate that comes under an efficient goods setting. The production of the goods comes under the efficient goods setting creates an added advantage in the production cost also it gains the competitive advantage

Therefore according to the given situation, the company has location economies realized

<span>P= -1000,000 +5000q - 0.25q2

q= 30n + 0.01n2

n = 20

substituting for q in P

P= -100,000 + 5000(30n+0.01n^2) - 0.25(30n+0.01n^2)

dp/dn = 5000*30+2*0.01*5000 - 0.25*2(30n+0.001n^2)+30+2*0.01n

dp/dn = 0.005n^2 +85.02n+150030

substituting for n=20 and solving

dp/dn = 151,732</span>

The essential rule that makers utilize to figure out what blend of work and capital conveys yield at the least expense is cost minimization. Cost minimization is the primary guiding principle that producers use to determine which combination of labor and capital produces the most output at the lowest cost.

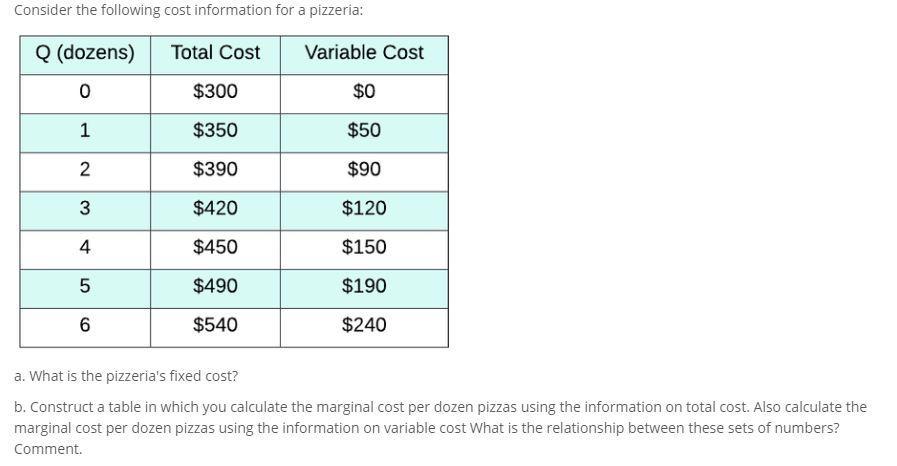

a) Because the total cost less the variable cost, the fixed cost is $300.

At a result of nothing, the main expenses are fixed expenses.

B) The change in total cost for each additional output unit is equal to marginal cost. Additionally, it is equivalent to the variation in variable cost for each additional output unit. As the quantity changes, the fixed cost does not change, so total cost equals the sum of variable cost and fixed cost. As a result, the increase in variable cost is proportional to the increase in total cost as quantity increases.

<h3>What is the formula for reducing costs?</h3>

The marginal product of capital is equal to the marginal product of labor divided by the rental price of capital in the cost minimization formula.

To learn more about Cost minimization here

brainly.com/question/13069227

#SPJ1

Answer:

The correct answer is a. a waste of available labor.

Explanation:

Productive efficiency (also known as technical efficiency) occurs when the economy is using all its resources efficiently, producing maximum production with minimum resources. The concept is illustrated in the Production Opportunity Frontier (FPP) in which all points of the curve are the points of maximum productive efficiency (that is, no more products can be achieved from the present resources).

This happens when the production of an economic good is achieved at the lowest possible cost, given the production of another good (s). In other words, when it is achieved, given the need to produce other goods, the highest possible productivity of a good. In a situation of long-term equilibrium for markets in perfect competition, it is where the average cost is the base on the average of the total cost curve, that is, the cost curve where CM = A (T) C.