The answer is <span> consideration

</span><span> consideration in business refers to the factors that sellers or buyers take into account when doing a certain transaction.

</span>In this particular case the delivery payment will be considered by hayden to determine the price in order to obtain the profit that she desired from the transaction.

Answer:

A saver buys a bond a corporation has just issued so it can purchase capital.

Explanation:

Direct finance is the process of financing in which the borrower borrows thd fund directly from the financial institution without involving the third party i.e intermediate, broker, etc

In the question, the option b is correct as it derives that a saver could purchase a bond since the corporation issued it so the capital could be purchased

hence, the second option is correct

Answer:

Through offering unique goods and services, entrepreneurs break away from tradition and reduce dependence on obsolete systems and technologies. This can result in an improved quality of life, improved morale, and greater economic freedom.

Explanation:

Answer:

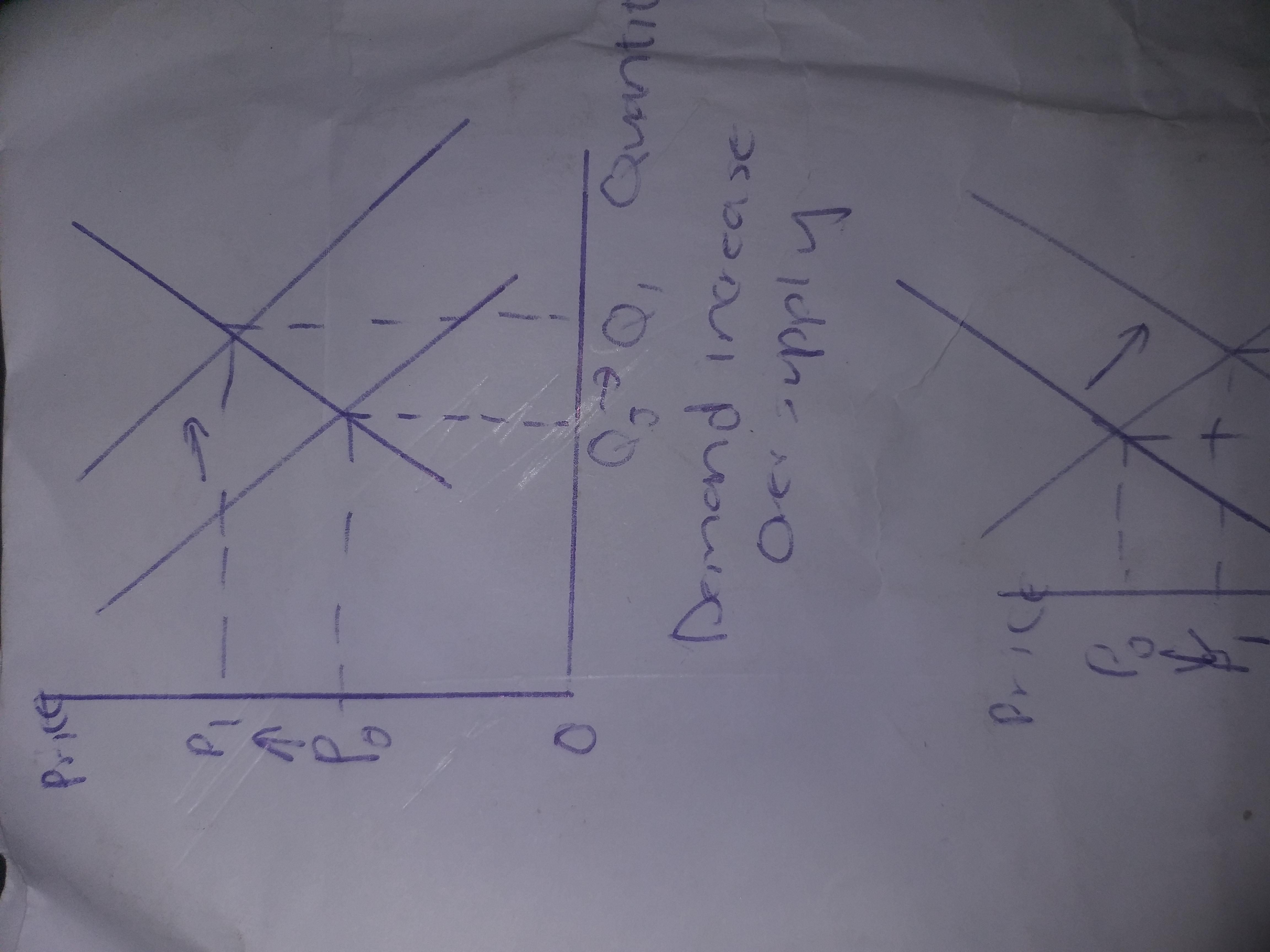

Up

Explanation:

When there aren't enough goods in the market, it means that the demand for goods exceeds its supply.

When there's excess demand over supply, prices rise.

When there's excess supply over demand, prices fall.

I hope my answer helps you.