Answer:

PART A

A constructive receipt is a term often used in both accounting and taxation to describe the taxation of an income even when the income had not been received by the person being taxed.

IMPORTANCE OF CONSTRUCTIVE RECEIPTS

It guarantees the early payment of taxes without undue delays from the tax payer.

It ensures effective taxation by effective tracking of the tax payers.

PARTB

(B) Under the concept of constructive receipt, income is taxed when it becomes available to the tax payer. The taxpayer cannot defer the tax by refusing to accept payment.

Explanation:

Constructive reciept is of great importance and relevance in the field of cost accounting and taxation,it guarantees early payment of taxes and effective tracking of tax payers by the regulatory or taxation bodies.

Under the concept of constructive reciept, income is taxed when it becomes available to the tax payer and it can not be deferred by refusing to accept payment.

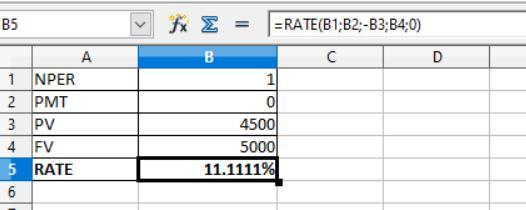

Answer:

11.11%

Explanation:

For computing the annual percentage rate (APR) we need to apply the RATE formula i.e to be shown in the attachment below.

Given that,

Present value = $5,000 × (100 - 10%) = $5,000 × 90% = $4,500

Future value or Face value = $5,000

PMT = 0

NPER = 1

The formula is shown below:

= -Rate(NPER;PMT;-PV;FV;type)

The present value come in negative

So, after applying the formula, the APR is 11.11%

Answer: $44,000<span>

<span>The tax laws state that any payments (except PUNITIVE

DAMAGES) on the account of a physical injury or physical sickness are non-taxable.

Damages that taxpayers can receive relating to emotional distress are also non-taxable.

Punitive damages however are fully taxable, because they are intended to penalize

the harm-doer rather than to compensate the taxpayer for injuries.</span></span>

Answer:

RAW DATA GAP, INC

statement of stockholders' equity

for the year ended January 29th, 2011

![\left[\begin{array}{cccccc}&$C Stock&$R/E&$OCI&$ Treasury Stock&$Total\\$Balance Jan 1&2990&10815&155&-9069&4891\\$Net Earnings&&1204&30&&1234\\$Dividends&&-252&&&-252\\$sale of stcok&&&&4&4\\$purchase of stock&&&&-1797&-1797\\$Balance, Dec 31&2990&11767&185&-10862&4080\\\end{array}\right]](https://tex.z-dn.net/?f=%5Cleft%5B%5Cbegin%7Barray%7D%7Bcccccc%7D%26%24C%20Stock%26%24R%2FE%26%24OCI%26%24%20Treasury%20Stock%26%24Total%5C%5C%24Balance%20Jan%201%262990%2610815%26155%26-9069%264891%5C%5C%24Net%20Earnings%26%261204%2630%26%261234%5C%5C%24Dividends%26%26-252%26%26%26-252%5C%5C%24sale%20of%20stcok%26%26%26%264%264%5C%5C%24purchase%20of%20stock%26%26%26%26-1797%26-1797%5C%5C%24Balance%2C%20Dec%2031%262990%2611767%26185%26-10862%264080%5C%5C%5Cend%7Barray%7D%5Cright%5D)

Explanation:

We list each equity concept and writetheir change and net effect on the total equity

Answer: A. All of these

Explanation: Change Control is the process companies uses to document, identify and authorize changes to an environment or process. It assists in reducing the chances of unauthorized modifications, disruptions and errors in the system/process and therefore follows a specific pattern towards its implementation. This would include: Change request identification, assessment, analysis, approval or rejection, and finally implementation. All these from start to finish is usually documented in the change request log.