Answer: A. Goal B

Explanation: Goal B is to be accomplished first. This is because on a timeline, the events closest to the present are on the left, and the events that happen far in the future are on the right.

P=present value

F=future value=500

n=number of years=2

i=annual interest rate=3%

We have

F=P(1+i)^n

=>

P=F/(1+i)^n

=500/(1.03^2)

= 471.30 to the nearest cent

Answer:

$77,760

Explanation:

After adjustment items of expenses will be deducted from the Net income, and items of income will be added to the net income.

Item of expenses = unpaid salary + Prepaid insurance (Expired)

Item of income = Interest earned + revenue

Net income after deduction = 77,600 - 795 - 555 + 755 + 755

Net income after deduction = $77,760

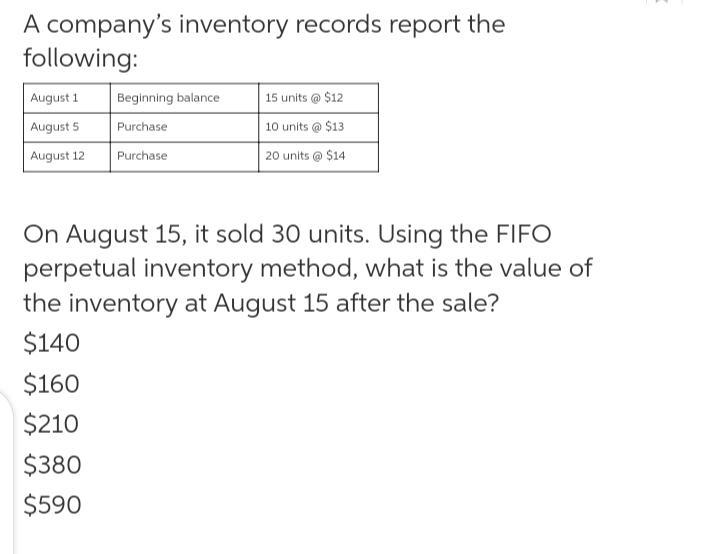

Answer: $210

Explanation:

When using the First In First Out (FIFO) method of Inventory Valuation, the company sells the goods that it acquired earliest first and then sells the goods acquired later last.

This company sold 30 units on August 15.

That would mean that using FIFO, the company sold all of its August opening inventory of 15 units. It also sold all 10 units purchased on August 5th and then sold 5 units from the August 12th purchase of 20 units.

= 15 + 10 + 5

= 30 units

This means that the only units left are;

= 20 - 5

= 15 units of the August 12th purchase are left.

Units cost $14 each.

Value of Inventory after sale = 15 units * 14

= $210

Answer:

Common stock issue price = 550 shares $5 par value

Common stock issue price = $2.750

Preferred stock issue price = $18,000

Par value of preferred stock = 300 shares * $15

Par value of preferred stock = $4,500

Paid in excess of par value of preferred stock = $18,000 - $4500

Paid in excess of par value of preferred stock = $13,500