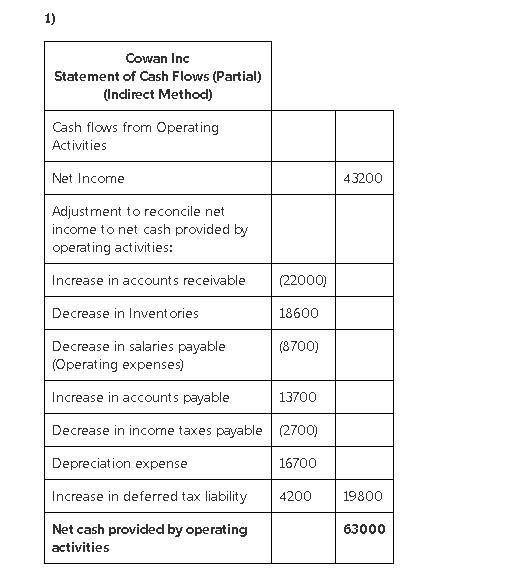

1-

Cowan Inc

Statement of Cash Flows (Partial)

(Indirect Method)

Cash flows from Operating Activities

Net Income 43200

Adjustment to reconcile

net income to net cash

provided by operating activities:

Increase in accounts receivable (22000)

Decrease in Inventories 18600

Decrease in salaries payable

(Operating expenses) (8700)

Increase in accounts payable 13700

Decrease in income taxes payable (2700)

Depreciation expense 16700

Increase in deferred tax liability 4200 19800

Net cash provided by operating activities 63000

2-

Cowan Inc

Statement of Cash Flows (partial)

(Direct Method)

Cash Flows from Operating Activities:

Cash Received from Customers (372700-22000) 350700

Cash paid to suppliers (221800-18600-13700) 189500

Operating Expenses Paid (80800+8700-16700) 72800

Taxes Paid (26900+2700-4200) 25400 287700

Net cash provided by operating activities 63000