Answer:

Option e: Increased opportunities for growth

Explanation:

Global trade is simply the exchange of goods between different countries.Trade is an exchange of items between people or countries.Countries are able to obtain goods they need from other countries.

four major risks in international business includes Country risk, commercial risk, cross-cultural risk, and currency risk.

Increased opportunities for growth is not an effect of risk in global trade.

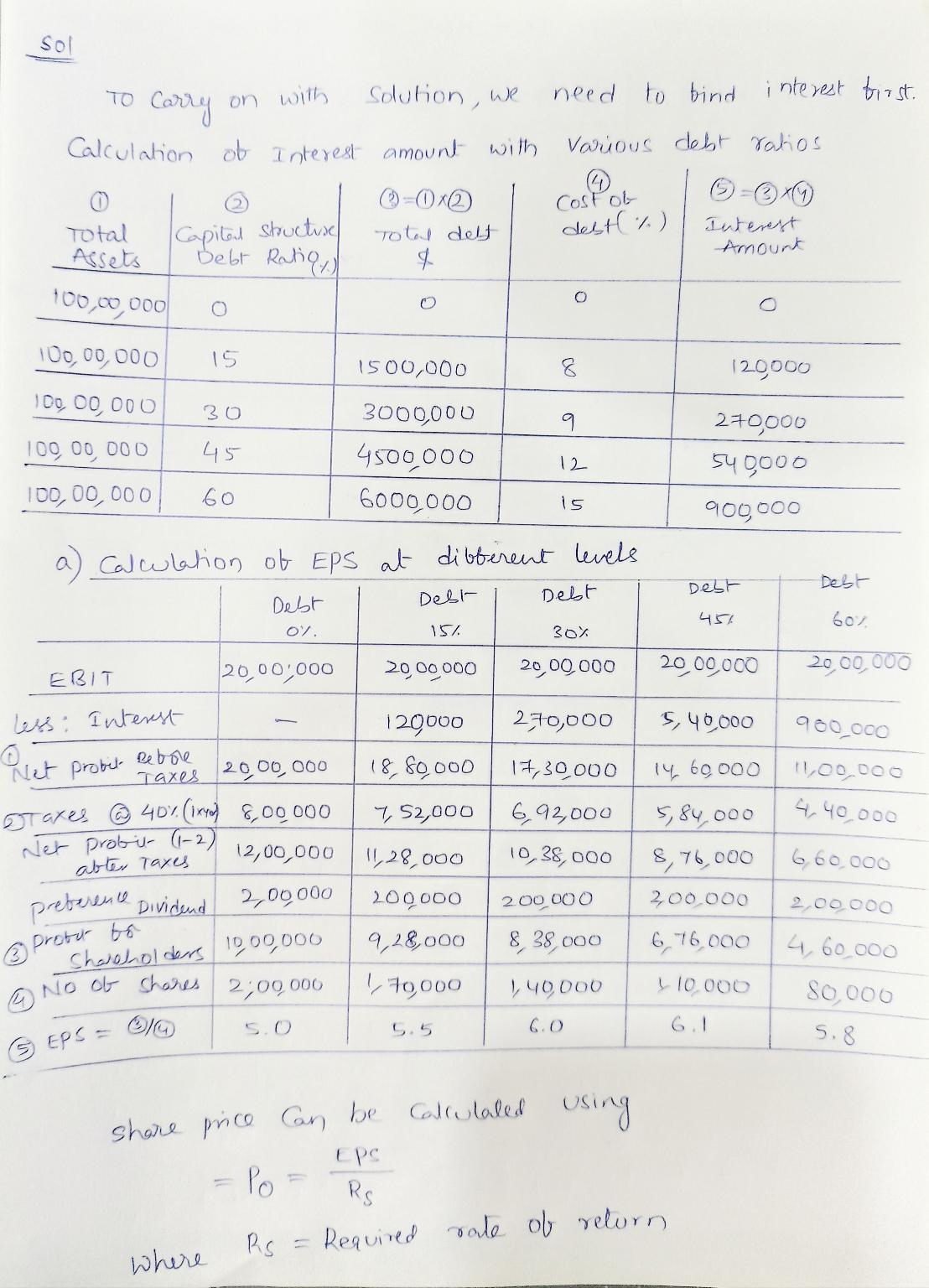

Answer:

Explanation:

The two attached pictures shows the explanation for this problem. I hope it help you. Thank you

The answer is "A) the popularity of electronic communication and the Internet".

Electronic communication provides the convenience for people. It leads the conventional newspaper and mail substituted by the electric one. The newspaper has been substituted by the electronic news. The conventional mail has been substituted by<span> social media and e-mail.</span>

Answer:

Eurenasia is a country that has frequently been assigned low macro-assessment ratings of country risk in the recent past due to its tendency to war with neighboring nations. MNC A is considering the establishment of a subsidiary to manufacture personal computers, while MNC B is considering the establishment of a subsidiary to manufacture tanks. Which of the two MNCs is likely to be less affected by the low macro-assessment?

Option B is correct - MNC B will be less affected by low macro-assessment.

Explanation:

Due to the tendency of Eurenasi to war with neighboring countries, the manufacture of tanks by MNC B will be less affected by low macro-assessment because, during war periods, tank sales will increase. Whereas, Low macro assessment will affect MNC A because it selling computers will be affected by war.

Therefore, Option B is correct - MNC B will be less affected by low macro-assessment.

Intends to create opportunities for performance and communication improvement makes the most sense to me