<span>Organic foods is using a growth strategy. A growth strategy is a strategy companies use when they want to grow their product depth, customer basis or product knowledge. There are four broad growth strategies to help a company achieve success. The four main growth strategies are </span>diversification, product development, market penetration, and market development.

Variable cost remains constant per unit at various levels of activity

Answer:

The correct answer is

D. -2 percent, which is the nominal interest rate minus the inflation rate.

The real interest rate equals D. the nominal interest rate minus the inflation rate.

Explanation:

The real interest rate formula is

<u>Real interest rate =Nominal interest rate - Inflation rate

</u>

Inflation rate=6 %

Nominal interest rate = 4%

Real rate of return =4% - 6 %

Real rate of return = -2%

D. -2 percent, which is the nominal interest rate minus the inflation rate.

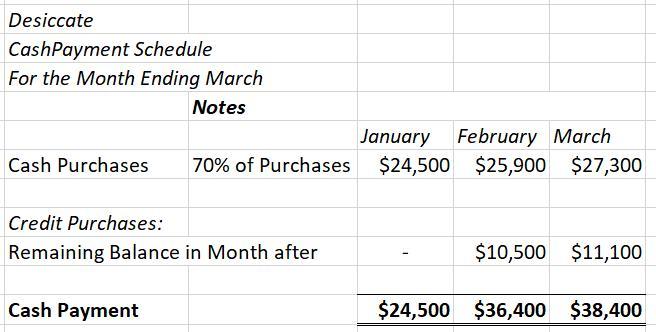

Answer:

$38,400

Explanation:

<em>1. Cash Purchases:</em>

The total purchases in the month of March is of $35,000.

It is given that 70% of Purchases are for cash.

Hence, 70% of $35,000 would be;

$39,000 x 0.70

$27,300

<em>2. Credit Purchases:

</em>

Remaining Balance of Purchases from the month of February:

For the month of February Cash Purchases can be calculated as follows;

$37,000 x 0.70

$25,900

Remaining Balance to be paid in March for the month of February can be calculated as follows;

$37,000 - $25,900

$11,100

<em>3. CASH PAYMENT for PURCHASES in MARCH:</em>

Cash Purchases = $27,300

Credit Purchases = $11,100

Hence;

<em>Cash Payment for purchases in March = Cash Purchases + Credit Purchases

</em>

Cash Payment for purchases in March = $27,300 + $11,100

Cash Payment for purchases in March = $38,400

The team dysfunction that is addressed by SAFe with the help of business owners is the lack of accountability.

<h3>What is the loss of accountability?</h3>

This can be defined as the scenario that occurs where people fail to take responsibilities for their lack of actions.

This may impede the growth of a team. Therefore it is very necessary that this is addressed to avoid issues.

Read more on accountability here:

brainly.com/question/980342

#SPJ12