By definition we have that the capital is equal to the Assets minus the liabilities.

In other words, we have:

C = A-P

Where,

A = Assets

P = Liabilities

C = Capital

Clearing assets:

A = C + P

A = 368000 + 186000

A = 554000

answer:

The assets are $ 554,000

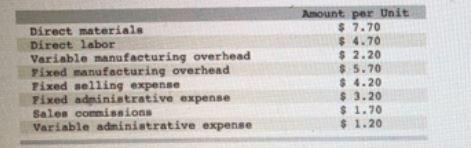

Based on the details given, the following are true:

- 1. Incremental manufacturing cost = $14.60

- 2. Incremental cost = $17.50

<h3>Incremental manufacturing cost if production increased from 20,250 to 20,251</h3>

The fixed cost will not change as the production amount is still below 24,500 units. Incremental manufacturing cost will therefore be:

= Direct material + Direct labor + Variable overhead

= 7.70 + 4.70 + 2.20

= $14.60

<h3>Incremental cost for increased from 20,250 to 20,251</h3>

This will include all costs that are not fixed.

= Incremental manufacturing cost + Sales commissions + Variable admin expense

= 14.60 + 1.70 + 1.20

= $17.50

Find out more on incremental manufacturing cost at brainly.com/question/8527680.

Answer:

d. $1050.

Explanation:

We multiply each account balance by the expected uncollectible amount and then addd them to get the expected total for doutful accounts

![\left[\begin{array}{cccc}Date&Amount&Expected&uncollectible\\$not due&10000&0.02&200\\$up to 30&5000&0.05&250\\$up to 60&3000&0.1&300\\$more than 61&800&0.5&400\\&&Total&1150\\\end{array}\right]](https://tex.z-dn.net/?f=%5Cleft%5B%5Cbegin%7Barray%7D%7Bcccc%7DDate%26Amount%26Expected%26uncollectible%5C%5C%24not%20due%2610000%260.02%26200%5C%5C%24up%20to%2030%265000%260.05%26250%5C%5C%24up%20to%2060%263000%260.1%26300%5C%5C%24more%20than%2061%26800%260.5%26400%5C%5C%26%26Total%261150%5C%5C%5Cend%7Barray%7D%5Cright%5D)

Balance of the allowance account: 100

The expense will be the adjustment made on the allowance to get the expected balance of 1,150

1,150 - 100 = 1,050

we increase the allowance bu 1,050 to get our expected uncollectible fro maccounts receivable agaisnt the bad debt expense ofthe period.

Business functions are the activities carried out by an enterprise; they can be divided into core functions and support functions. Core business functions are activities of an enterprise yielding income: the production of final goods or services intended for the market or for third parties