Answer:

The correct answer is B: $5,600

Explanation:

Giving the following information:

Schager Company purchased a computer system for $40,000. The estimated useful life is 10 years, and the estimated residual value is $5,000.

Double-declining balance method= Netbook value* (2/useful life in years)

Year 1:

Double-declining balance method= (40000-5000)*(2/10)= $7000

Year 2:

Double-declining balance method= (35000-7000)*0.20= $5,600

Answer:

I will use images and details from credible websites, which will boost my own credibility and support my claim. I will also use charts and graphs from trusted web resources, such as government and university sites, to make my supporting evidence clear

Explanation:

I took the test

Brainiest???

Answer:

B) performing stage of group development.

Explanation:

The stages in group development are

- forming.

- storming.

- norming.

- performing.

- adjourning.

In the forming stage, the project team members get to know each other and lay the basis for project and team ground rules.

In the storming stage, features the start of conflict as team members begin to resist authority and demonstrate hidden agenda.

In the norming stage, members agree on operating procedures and seek to work together.

In the the performing stage, finally committing to the project development process. Group members work to accomplish the project and display a level of competence.

In the adjourning stage, once their work is done, group is disband.

Answer:

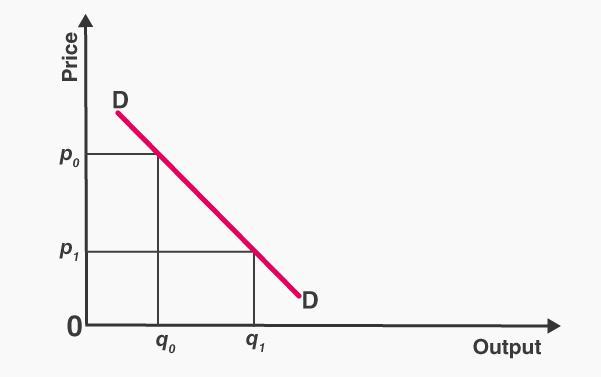

the sum of all prices that the individual buyers are willing and able to pay for each possible quantity of the good.

Explanation:

Market demand refers to the sum of the individual demand for a commodity from all buyers in a given market.

A market demand curve is therefore a graph that shows the the sum of the individual demand for a commodity from all buyers in the market.

Therefore, the correction option is "the sum of all prices that the individual buyers are willing and able to pay for each possible quantity of the good".

Note that the market demand curve is a downward sloping curve due to the fact that there is a negative relationship between price and quantity demanded. That is, as price increases, the quantity demanded decreases. On the other hand, as price decreases, the quantity demanded increases.

Also note that an example of a market demand curve is given in the attached graph. From the graph, it can be seen that when price is  , quantity demanded is

, quantity demanded is  . But when price falls to

. But when price falls to  , quantity demanded increased to

, quantity demanded increased to  . This shows the negative relationship between price and quantity demanded as explained above.

. This shows the negative relationship between price and quantity demanded as explained above.

Answer: In market economies, buyers of inputs know that sellers want to earn profits.

Explanation: In a command economy, the state decides about what goods are to be produced, how much they must be produced and at what price they must be distributed in the society. While, in a market economy decisions about investment and production are determined by the forces of demand and supply. A command economy focuses on social welfare and equal distribution. While a market economy is driven by the profit motive. Thus, it is easy for firms to buy inputs in a market economy than in a command economy. In market economies, buyers of inputs know that sellers want to earn profits.