Answer:

A. Market Timing

Explanation:

Based on the information provided within the question it can be said that the term being described within the question is called Market Timing. Like mentioned in the question this term refers to a strategy of buying and selling different financial assets, usually by trying to take advantage of price discrepancies in the short term.

Answer:

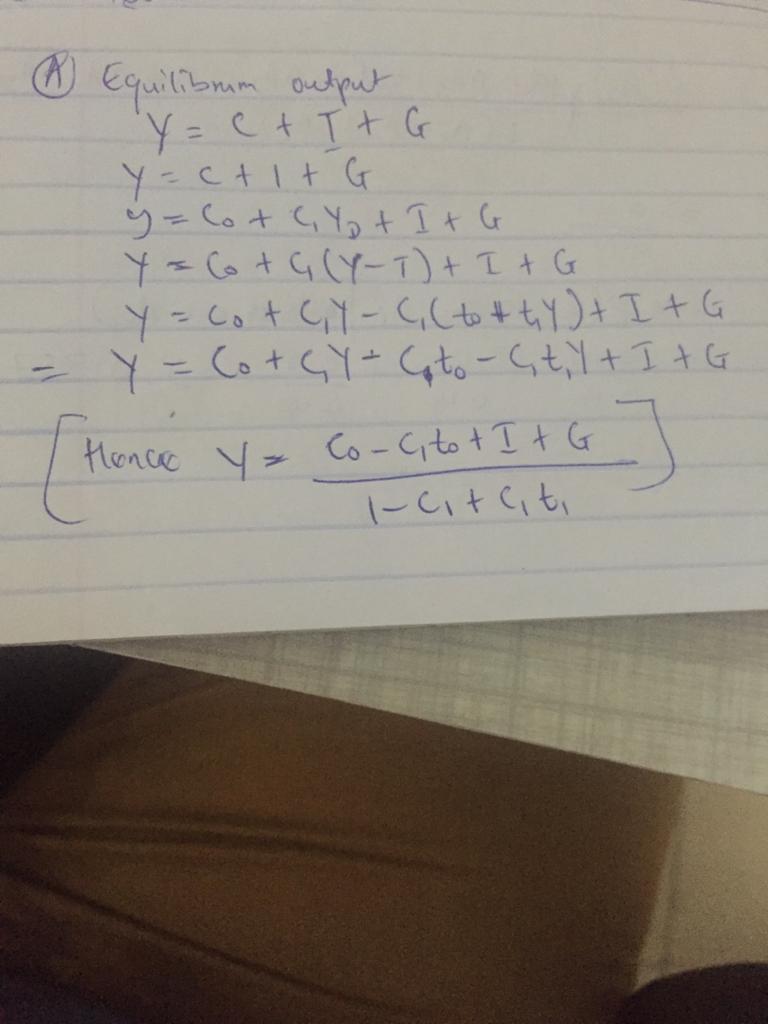

A) attached below

B)

C) The fiscal policy is called an automatic stabilizer because the taxes are dependent on the level of income and also the output of the multiplier is more stable because it doesn't respond to rapid changes in fiscal policies.

Explanation:

Given data:

C = Co + C1YD

T = t0 + t1Y

YD = Y - T

G and I are both constant

C1 lies between 0 and 1 while T1 lies between 0 and 1

A ) solving for equilibrum output

attached below

B) The multiplier

Multiplier =

The economy responds to changes in autonomous spending when t1 is 0 but responds less when t1 is positive, this is because the more positive t1 is the lower the multiplier value

c) The fiscal policy is called an automatic stabilizer because the taxes are dependent on the level of income and also the output of the multiplier is more stable because it doesn't respond to rapid changes in fiscal policies.

Answer:

The Marston Corp. disbursement float is $ (16,768.00)

Explanation:

The firm writes 28 checks a day for an average amount of $398 each, is equal to say = 28 * $398 = $ 11,144.00 . If these checks generally clear the bank 3 days after they are written, then = $ 11,144.00 * 3 = $ 33,432.00

And, the firm generally receives 40 checks with an average amount of $502 each, is equal to say = 40 * $502 = $ 20,080.00 . If the deposited amounts are available after an average of 2.5 days, then = $ 20,080.00 * 2.5 = $ 50,200.00

The Marston Corp. disbursement float is = $ 33,432.00 - $ 50,200.00 =

$ (16,768.00)

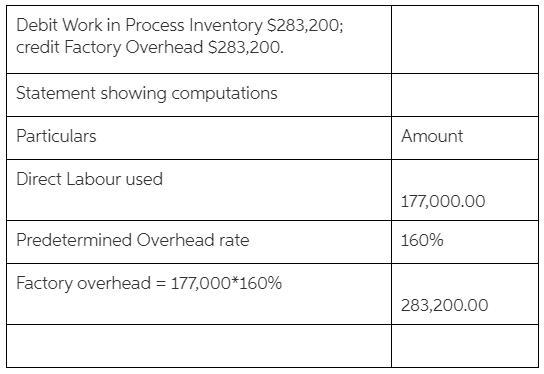

Answer:

Detailed solution is given in tabular form in the end for better understanding.