I believe the answer is A: Current ratio. It’s the only one that makes sense.

<span>Organic foods is using a growth strategy. A growth strategy is a strategy companies use when they want to grow their product depth, customer basis or product knowledge. There are four broad growth strategies to help a company achieve success. The four main growth strategies are </span>diversification, product development, market penetration, and market development.

A company has net income of $ 225,000 and declares and pays dividends in the amount of $ 75,000 .

c. An increase of $ 150,000 is the net impact on retained earnings is the correct option.

Income is the consumption and savings opportunity that a business captures within a specific time frame, usually expressed in money. Income is difficult to define conceptually and definitions vary by region.

For most people, income means gross income in the form of wages and salaries, return on investment, pension payments, and other income.

The definition of income is the amount of money received by an individual, group or business during a specified period. An example of income is an annual salary of $70,000.

Learn more about income here:brainly.com/question/25745683

#SPJ4

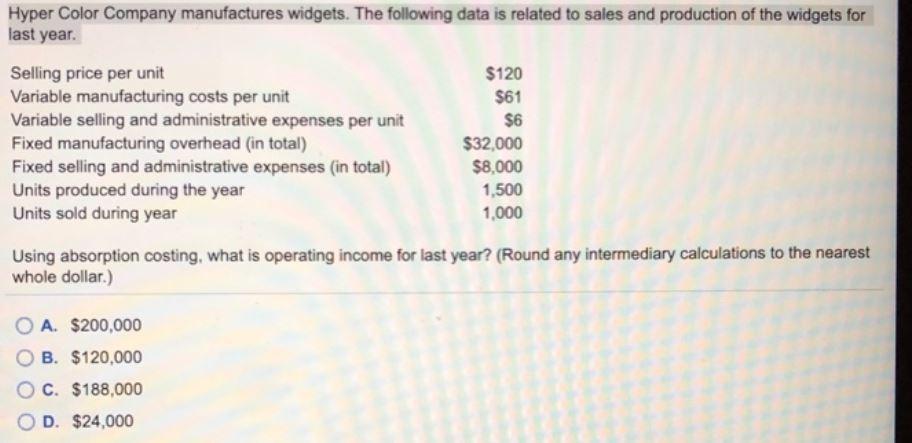

Answer: $24,000

Explanation:

Operating income under absorption costing:

= Sales - Cost of goods sold - Selling and admin expenses

Cost of goods sold = Variable production cost + Fixed production cost

= (61 * 1,000 units sold) + (32,000 / 1,500 units produced * 1,000 units sold)

= $82,333

Selling and admin expenses:

= Variable + Fixed

= (6 * 1,000) + 8,000

= $14,000

Operating income = (120 * 1,000) - 82,333 - 14,000

= $23,667

= $24,000

Answer:

50,000 pounds of chicken meat

Explanation:

If 10,000 packages of chicken sausages were produced, the estimated amount of chicken meat and machine hours would equal:

- chicken meat = 10,000 packages times 5 pounds per package = 50,000 pounds of chicken meat

- machine hours = 10,000 packages times 2 hours per package = 20,000 machine hours