<span>Multinational corporations are also referred to as </span>transnational corporations. Hope this helps!!

Answer:

Option C Differentiating the market offering to create superior customer value

Explanation:

The reason is that when the product are differentiated from the rest of the products in the market, it creates a sense of superiority among products because of its quality, uniqueness and exceptional things that the company offer with the product. Due to differentiated strategy, the company is able to sell at a higher price which earns greater profit for the company.

Answer:

TRUE

Explanation:

- Business globalization means designing marketing strategies as if they were a single entity for the whole planet or large parts of it.

In an increasingly interdependent and incorporated global economy, merchandising globalization is a complementary term combining the promotion and sale of goods and services.

It renders stateless, wall-less businesses an essential marketing and cultural tool with the internet.

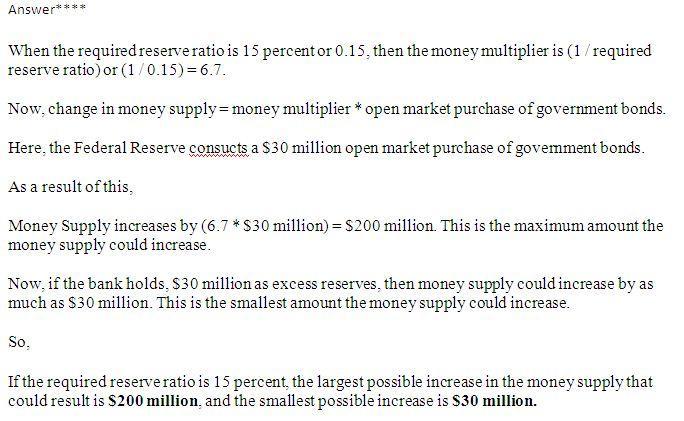

Answer

a. 200 million

b. 30 million

The answer and procedures of the exercise are attached in the image below.

Explanation

Please consider the data provided by the exercise. If you have any question please write me back. All the exercises are solved in a single sheet with the formulas indications.

Answer:

The surrender cash value is used for the extended term option.

Explanation:

This is where the nonforfeiture clause comes to policyholders aid. The nonforfeiture clause allows the policy holder who has not made payment of premiums within the grace period to be able to get the cash value of his whole life policy(with already paid premiums), recovered either by cash or extended term option or any other agreement made prior. The cash value of his whole life policy could be applied to the extended term option, allowing the policy holder to get a term insurance policy worth the value of his surrender whole life policy minus any loans against it.