Answer:

If management decides to eliminate this product line, the company’s net income will reduce by $22,000

Explanation:

<em>A product should be shut down if doing so would make the savings in fixed costs associated with the product to exceed the lost contribution. Other wise , the product should remain.</em>

<em>In a shut down decision , the following relevant cash flows should be considered:</em>

- <em>Lost contribution from the product to be shut down</em>

- <em>Savings in fixed directly attributable to the product under consideration.</em>

$

Lost contribution from shut down (100,000)

Savings in fixed cost (60% × 130,000) <u> 78,000</u>

Net loss from shut down <u> (22,000)</u>

Net loss from shut down = $(22,000)

If management decides to eliminate this product line, the company’s net income will reduce by $22,000

Explanation:

you can come to India I think here you will get it

Answer:

E.match its core competencies.

Explanation:

The Mayo Clinic in Minnesota is known for top-quality medical care and focusing its efforts on satisfying customer needs that match its core competencies.

every organization has is desire goals and vision.

the goals and vision of Mayo clinic is satisfying customer need which made them provide all the social amenities and medical equipment and infrastructure needed for quality treatment of patient.

with this core competencies : its makes then increase and advance there there establishment to other countries.

Answer:

Attending

Explanation:

There are four steps in the risk negotiation cycle that includes attending, sensemaking, transforming and maintaining.

While assessing and analyzing the forms of communication and the workers orientations with respect to identify the sources reflects the attending phase whether the employees attend the orientations and according to that the analyzed could be done

Therefore this is an attending phase

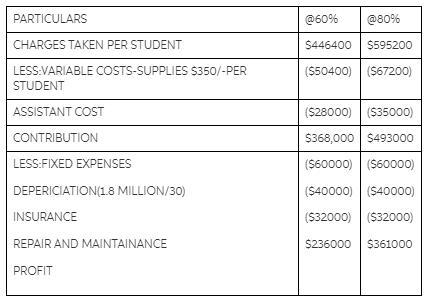

Answer:

IF WOOL MEN CHARGES $3100 PER STUDENT,THEN CONTRIBUTION PER STUDENT=

CHARGES PER STUDENT =$3100

LESS:VARIABLE COST

SUPPLIES ($350)

ASSISTANT SALARY ($155)

($7000/45)

CONTRIBUTION $2595

COST PER STUDENT:

SUPPLIES $350

OFFICE ($7000/45) $155

INSURANCE ($40000/240*) $167

REPAIR ($32000/240) $133

AND MAINTENANCE

DEPOSIT ($60000/240) $250

TOTAL $1055

Explanation:

The given table will elaborate it more.