Answer:

$291,000

Explanation:

The computation of the manufacturing overhead is shown below:

= Indirect materials requisitioned for use in production + Indirect labor wages incurred + Depreciation recorded on factory equipment + Additional manufacturing overhead costs incurred

= $45,000 + $119,000 + $44,000 + $83,000

= $291,000

All indirect cost are to be consider as a manufacturing overhead. So, we consider this costs only.

Answer:

8.27%

Explanation:

Data provided in the question:

Current price = $36.72

Annual dividend paid, D0 = $2.18

Dividend growth rate, g = 2.2% = 0.022

Now,

Cost of Equity = [ (Dividend For Next Year) ÷ Current Price ] + Growth rate

= [ ( D0 × ( 1 + g ) ) ÷ $36.72 ] + 0.022

= [ ( $2.18 × ( 1 + 0.022 ) ) ÷ $36.72 ] + 0.022

= [ 2.22796 ÷ $36.72 ] + 0.022

= 0.06067 + 0.022

= 0.08267

or

= 0.08267 × 100% = 8.267% ≈ 8.27%

Answer:

The correct answer is A. A fixed ratio reinforcement schedule

Explanation:

When we perform an operant conditioning following a fixed interval reinforcement program, we administer to the subject the reinforcing stimulus only when a certain time has elapsed since the last presentation of the reinforcement, that is, with a constant time interval, for example, every minute. If the time interval is not constant but variable, that is once every minute, another every three, another every two, ..., then we have a variable interval reinforcement program.

If we want to create an operant behavior in a subject, we can administer the reinforcing stimulus only when the subject performs a certain number of times the behavior in question, for example every three times; in that case we have a fixed rate reinforcement program. If we prefer to administer the reinforcement when the subject performs a variable number of behaviors (for example, sometimes every three behaviors, sometimes every two, sometimes every four) we have a variable rate reinforcement program.

Answer

The answer and procedures of the exercise are attached in the following archives.

Explanation

You will find the procedures, formulas or necessary explanations in the archive attached below. If you have any question ask and I will aclare your doubts kindly.

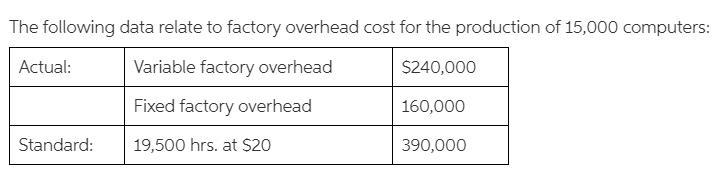

Answer:

Controllable Variance = $6,000 Unfavorable

Volume Variance = $4000 Unfavorable

Factory overhead cost variance = $10,000 Unfavorable

Explanation:

Controllable Variance = (Budgeted Factory Variable Overhead - Actual Factory Variable Overhead)

= ($234,000 - $240,000)

= $6,000 Unfavorable

Budgeted Factory Variable Overhead = ($394,000 - $160,000)

= $234,000

Volume Variance = (Standard Hours for Actual unit Produced - Standard Hour for normal Capacity) Fixed Factory Overhead)

=(19,500-20,000) × $8

= $4,000 Unfavorable

Controllable Variance = $6,000 Unfavorable

Volume Variance $4000 Unfavorable

Factory overhead cost variance = Controllable Variance + Volume Variance

= $6,000 + $4,000

= $10,000 Unfavorable