Answer:

There will zero economic profits in the long run.

Explanation:

Monopolistic competition is a market structure where there is a large number of firms producing differentiated products. There is very low or no restriction on the entry and exit of firms in the market.

The market for plumbing services in a city is a monopolistic competition. An increase in the market demand will cause the price to increase. This will cause an increase in the profits of the existing firms.

In the long run, new firms will enter the market, increasing the market supply. This will cause the price level to decrease till all the firms are having zero economic profits.

<u>Solution and Explanation:</u>

<u>Moral Hazard </u>– It is a situation when a firm or an individual modify their behaviour once the person gets what one was desired to achieve; example, insurance, funding, etc.

<u>Adverse selection </u>- The firm does not information on the consumer, and, sells the product at lower price assessing a lower risk when more information would have made the seller ask for a higher price

a) Moral Hazard

The country changes its project plan after the World Bank extends the loan; if the World Bank has put in conditions that it be used only for a canal, then the loan cannot be used

Answer:

Instructions are listed below.

Explanation:

Giving the following information:

The members want to set up a perpetual fund to provide $100,000 for future replantings every 10 years. The interest rate is 5%.

I will assume that the money is deposited as a lump sum:

FV= PV* (1 + i)^n

PV= FV/ (1+i)^10

PV= 100,000 / 1.05^10= $61,391.33

Now, if n is 100 years:

PV= 100,000/ 1.05^100= $760.45

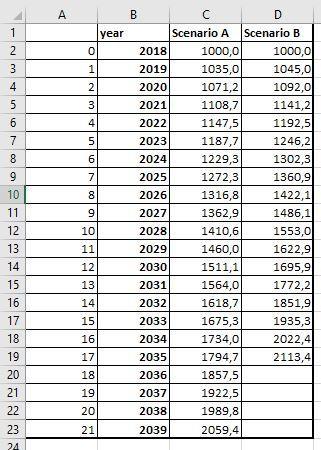

Answer:

2. 20 years under scenario A, versus 16 years under scenario B

Explanation:

It is clearer if I explained with an example:

Let suppose that a nation´s real GDP for 2018 was 1000. In scenario A you will have:

2019:1000*3.5%=1035

2020:1035*3.5%=1071,2

and so on, the same for scenario B

2019: 1000*4,5%= 1045

2020: 1045*4,5%= 1092

and so on.

I attached an excel table where you can see that: in the first scenario, between year 20 and 21 (2038 and 2039) the GDP will double and in the second one, between year 15 and 16 GDP will double. The answer is 2.

Both A and B so answer C.