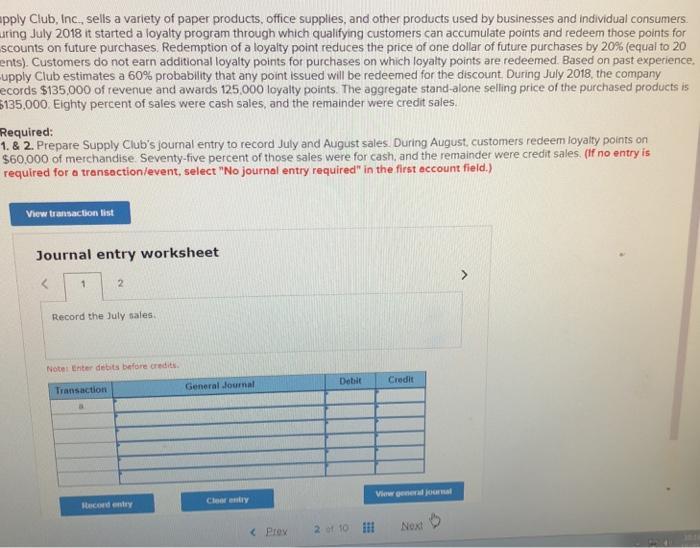

Answer: This question is not complete.

Explanation:

The full question can be seen in the picture while the solution is in the file attached below

Answer:

The interest revenue that should be reported in the first year, for two months from November to December, on 31 December is $3600.

Explanation:

According to the accrual basis of accounting, the revenues and expenses for a particular period should be recorded in the period to which they relate to rather then when they are received or paid. This means that although the interest will be received on March 1 of the next year, the interest revenue on note receivable for a period of two months from November to December should be recorded in the first year because it has been earned in the first year and it relates to it.

Interest revenue - first year = 270000 * 0.08 * 2/12 = $3600

1. Nikita creates an FSA ID

2. Nikita fills out the FAFSA online.

3. Colleges ask Nikita to verify the information in the FAFSA

4. Nikita rechecks the information she provided and makes a few corrections.

5. In about two weeks, Nikita receives a document called Student Aid Report (SAR)

6. Nikita receives financial aid award letters from various colleges.

Answer: Mortgage interest is a loan.

Explanation: