The stakeholder register entry is inadequate is a marketing leader.

<h3>Who is a stakeholder?</h3>

A stakeholder is a party that has an interest in a company and can either affect or be affected by the business.

A marketing leader is not an adequate entry in a stakeholder register. There are situations in which communicating to people face-to-face is the best way to get something accomplished.

When conversing with emotionally charged people on a complex topic, communication over text or email can be cumbersome and ineffective.

Learn more about stakeholder on:

brainly.com/question/4404879

#SPJ1

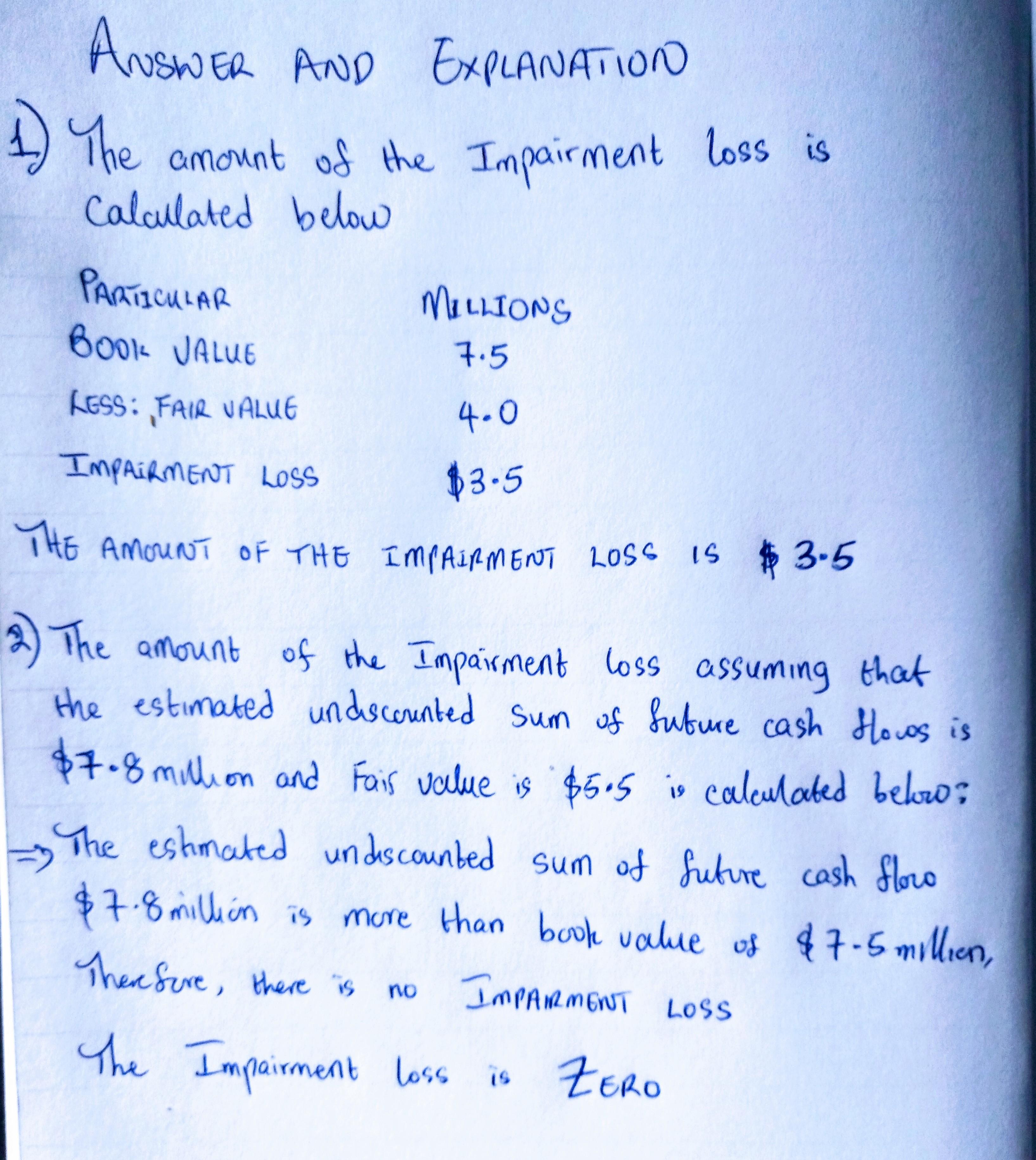

Answer and Explanation:

The answer and workings can be viewed in the snapshot below:

Answer:

Im so so sorry but I dont know how to do this

Explanation:

Answer:

Proofread for punctuation errors (it's a must!!), Jot down reasons that explain the bad news (I think), Organize your ideas (I think)

Explanation:

I think: Jotting down the reasoning helps/support the information (specifically) the bad news. Organizing your ideas helps to keep everything you write on track and ideas you want to mention always start from check-point A to check-point B and so forth.... (It's my thoughts of an answer)

Answer:

$3,765.26

Explanation:

Present value is the sum of discounted cash flows.

Present value can be calculated using a financial calculator

Cash Flow in year 1 = $ 820

Cash Flow in year 2 = 1,130

Cash Flow in year 3 = 1,390

Cash Flow in year 4 = 1,525

I = 10

PV = $3,765.26

To find the PV using a financial calacutor:

1. Input the cash flow values by pressing the CF button. After inputting the value, press enter and the arrow facing a downward direction.

2. After inputting all the cash flows, press the NPV button, input the value for I, press enter and the arrow facing a downward direction.

3. Press compute

I hope my answer helps you