Answer:

It is important to stand up to bullying for a number of reasons. You may think it's better to not get involved but staying neutral always helps the oppressor. You should not let someone suffer and watch as someone else puts them in physical or psychological pain every day, it is good to stand up for what is right. You may even make a life-long best friend. So stand up for what's right and don't stay neutral so the oppressor can continue to victimize someone.

Explanation:

Hope this helps! :)

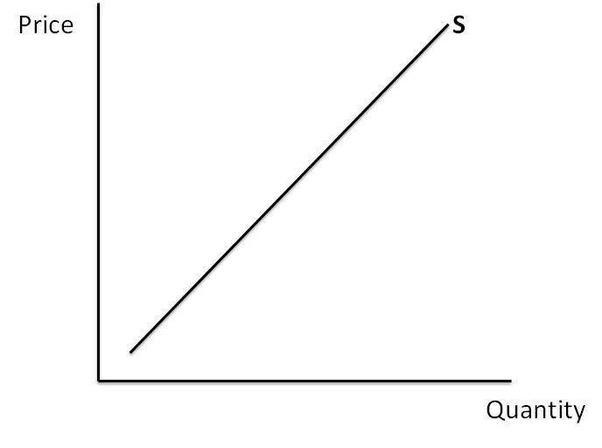

Answer:

A. slopes upward

Explanation:

(I will include a picture in the attachment to help with the explanation)

Slope upward represent the increase in quantity as the price goes up.

As the price of a product is increased, the potential profit that the producer can generate is also higher. Because of this, they become motivated to supply more product for the customers. They will increase their production output and increase the amount of distributions to the market.

This is why the slope will become upward like the picture above.

Answer:

my baby daddy.

Explanation:

I forgot to take the pill :(

Companies and consumers started to understand in the 1930s that using resources properly and efficiently was advantageous for both society and business. the green revolution sprang from this.

The green revolution is a broad movement that advances the concerns of environmentalists, or people who believe that it is important to preserve the integrity of the non-human world for both that reason and the survival of humans. Its membership is extraordinarily diversified, including academics, political activists, wealthy and impoverished individuals from all over the world, as well as followers of a wide range of religious ideologies. Global climate change has been a major issue for the green movement since the 1980s. The preservation of both multi-use undeveloped landscapes and natural regions, the protection of endangered species, and resistance to pollution are further issues.

Learn more about green revolution here

brainly.com/question/25077523

#SPJ4

Answer:

Explanation:

The journal entries are shown below:

(a) a $415 credit balance before the adjustment.

Bad debt expense A/c Dr $685

To Allowance for Doubtful Accounts $685

(Being bad debt expense recorded)

Since the allowance for doubtful debts have a credit balance so this amount will be deducted. The computation is shown below?:

= (Outstanding accounts receivable × uncollectible rate) - credit balance

= ($55,000 × 2%) - $415

= $1,100 - $415

= $685

(b) a $291 debit balance before the adjustment.

Bad debt expense A/c Dr $1,391

To Allowance for Doubtful Accounts $1,391

(Being bad debt expense recorded)

Since the allowance for doubtful debts have a debit balance so this amount will be added. The computation is shown below?:

= (Outstanding accounts receivable × uncollectible rate) + debit balance

= ($55,000 × 2%) + $291

= $1,100 -+$291

= $1,391