Answer:

It must be paid within one year or the operating cycle, whichever is shorter.

Explanation:

Current liabilities are short term obligations that a company needs to pay within the current financial year. Companies use current assets to offset their current liabilities. Examples of current liabilities include accounts payable, interest payable on outstanding loans, dividends payables, and long term debts maturing within the current financial year.

A business needs to monitor its levels of current liabilities to ensure it has sufficient current assets to pay them. There are situations where a company finds it necessary to obtain a loan to finance its current liabilities. The inability to pay current debts consistently may be indicative of more profound financial challenges within the organization.

The classic anthropological definition of culture is ---“that complex whole which includes knowledge, belief, art, law, morals, custom, and any other capabilities and habits acquired by man as a member of society”

What is the meaning of complex whole?

Whenever a relation holds between two or more terms, it unites the terms into a complex whole. Literature. The food industry as a complex whole requires an incredibly wide range of skills. If Othello loves Desdemona, there is such a complex whole as 'Othello's love for Desdemona'.

What is a complex culture?

a group of culture traits all interrelated and dominated by one essential trait: Nationalism is a culture complex.

How do you define culture and society?

A culture represents the beliefs and practices of a group, while society represents the people who share those beliefs and practices. Neither society nor culture could exist without the other.

Learn more about complex culture:

brainly.com/question/18512761

#SPJ4

Answer:

A. Matched Samples

Explanation:

Matched samples is a situation whereby participants are paired, sharing every other characteristics except the one under investigation. The idea behind this is to have more control over unwanted variables. In this case, the study is measuring two production methods and in order to control the unwanted variable and leave only the characteristic or variable under investigation which is the production method, the two method is carried out by the same workers each.

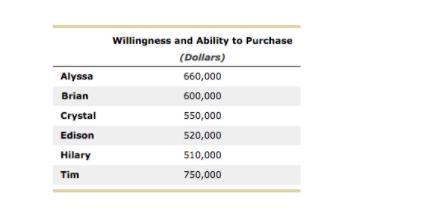

Answer:

a) will

d) crystal

Explanation:

Please find the information needed to answer this question in the attached image

Willingness to pay is the highest amount a consumer would be willing to buy a product. If the price of the good is below the willingness to pay, the consumer would purchase the good.

The three beachfronts were sold to Alyssa, Tim and Brian.

The new sale of the beachfront at $535,000 would be sold to crystal because her willingness to pay ($550,000) is higher than the price of the beachfront.

the consumer surplus from the purchase would be $550,000 - $535,000 = $15,000

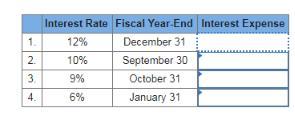

Answer:

the question is incomplete, so I looked for a similar one online:

December 31, year 1:

interest expense = $5,300,000 x 12% x 6/12 = $318,000

September 30, year 1:

interest expense = $5,300,000 x 10% x 3/12 = $132,500

October 31, year 1:

interest expense = $5,300,000 x 9% x 4/12 = $159,000

January 31, year 2:

interest expense = $5,300,000 x 6% x 7/12 = $185,500