The answer is: B, A boss who is respectful and cooperative. Hope this helped.

Answer:

Particulars Amount Explanation

Call options 1350000

Beta of stock 1.7

Delta 0.7

Market change 1% Implied stock change is 1.7

Stock changes by 1.7 1.19 Implied exposure on call

options on stock ( ie 1.7*0.7)

Amount of exposure 1606500 Derived by multiplying

1.19*1,350,000

Hence market index portfolio worth $1,606,500 should be bought , however the market index portfolio trade in multiples of 1000 hence $1,607,000 worth should be obtained to hedge the exposure

Explanation:

Answer:

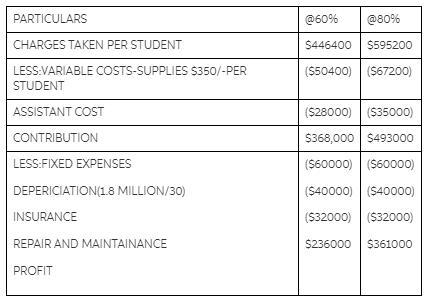

IF WOOL MEN CHARGES $3100 PER STUDENT,THEN CONTRIBUTION PER STUDENT=

CHARGES PER STUDENT =$3100

LESS:VARIABLE COST

SUPPLIES ($350)

ASSISTANT SALARY ($155)

($7000/45)

CONTRIBUTION $2595

COST PER STUDENT:

SUPPLIES $350

OFFICE ($7000/45) $155

INSURANCE ($40000/240*) $167

REPAIR ($32000/240) $133

AND MAINTENANCE

DEPOSIT ($60000/240) $250

TOTAL $1055

Explanation:

The given table will elaborate it more.

The value is what the company earned from profits. The company's income and revenue minus explict cost.