Answer:

The transferor does not maintain effective control over the transferred financial asset or third party beneficial interest in the asset.

Explanation:

The code for transfer of receivable provisions, allows creditor of a debt to have the right to transfer his/ her receivable right to another person, provided that the transaction is permitted by the law/ contract nature of business. Transfer of receivables permit the third person/ party to be included in the relationship that exist between debtor and creditor, and this allows him/ her to near the title of creditor.The receivable must be an existing one before the receivable transfer can be possible. It should be noted that for transfer of receivables be recorded as a sale, The transferor does not maintain effective control over the transferred financial asset or third party beneficial interest in the asset.

Answer:

The answer is: Rawl Co. should recognize the related revenue evenly over the contract year as the services are performed.

Explanation:

According to the conservatism principle, Rawl Co. should record revenues and assets only when you are sure that they will occur. So they should record revenue only as the service is provided on a monthly basis.

It should determine the monthly payment = $540 / 12 = $45 per month.

So at the end of every month, it should recognize $45 as revenue.

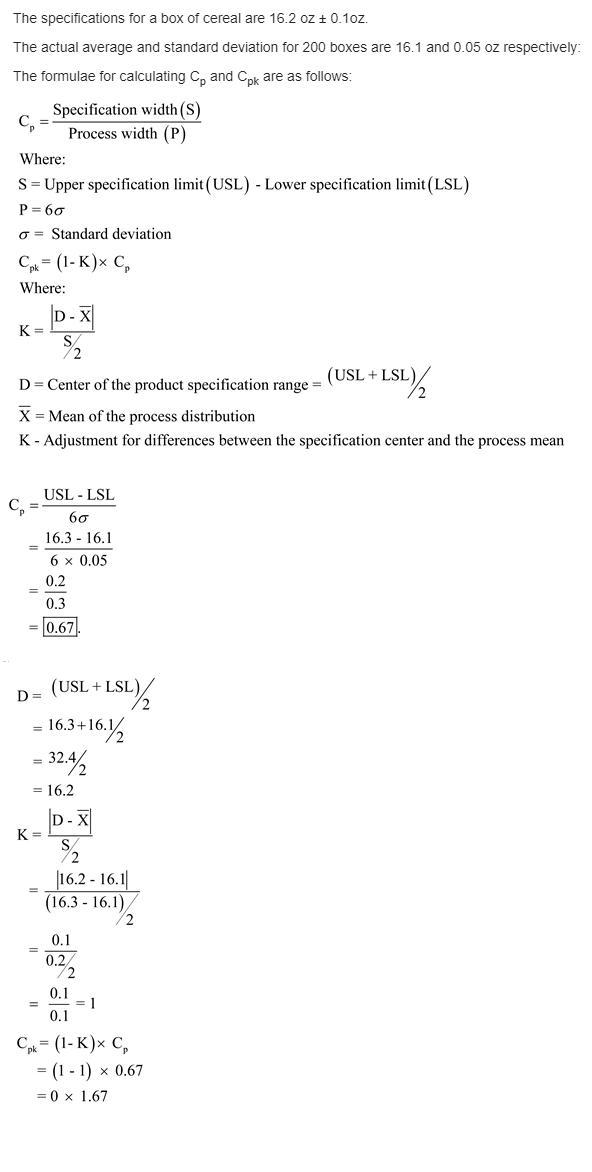

Answer

The answer and procedures of the exercise are attached in the following archives.

Explanation

You will find the procedures, formulas or necessary explanations in the archive attached below. If you have any question ask and I will aclare your doubts kindly.

<u>Answer: </u>Strengths and weaknesses

<u>Explanation:</u>

Situational analysis for a company is determined by the internal and external factors which can be said as SWOT analysis. Here the internal factors are strengths and weakness of the company. While the external factors are opportunities and threats. Situational analysis is an element of the marketing plan.

These internal and external factors show how the sales and profit of the company is affected in the market. The internal components of the company are helpful to identify the ways the company can improve its operations.