Liability insurance or legal liability

Who agrees to pay for certain types of losses in exchange for payments on a policy?

An insurer. An insurer is someone representing a company that is insuring someone else. When you are insured, you are paying for a policy and if you need to file a claim against your policy, the insurer will pay out the loss.

Answer

The answer and procedures of the exercise are attached in the following archives.

Explanation

You will find the procedures, formulas or necessary explanations in the archive attached below. If you have any question ask and I will aclare your doubts kindly.

The essential rule that makers utilize to figure out what blend of work and capital conveys yield at the least expense is cost minimization. Cost minimization is the primary guiding principle that producers use to determine which combination of labor and capital produces the most output at the lowest cost.

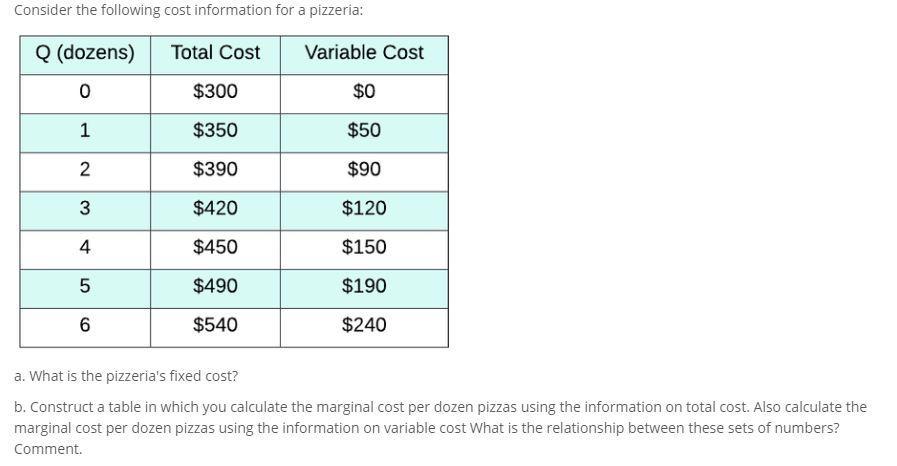

a) Because the total cost less the variable cost, the fixed cost is $300.

At a result of nothing, the main expenses are fixed expenses.

B) The change in total cost for each additional output unit is equal to marginal cost. Additionally, it is equivalent to the variation in variable cost for each additional output unit. As the quantity changes, the fixed cost does not change, so total cost equals the sum of variable cost and fixed cost. As a result, the increase in variable cost is proportional to the increase in total cost as quantity increases.

<h3>What is the formula for reducing costs?</h3>

The marginal product of capital is equal to the marginal product of labor divided by the rental price of capital in the cost minimization formula.

To learn more about Cost minimization here

brainly.com/question/13069227

#SPJ1