Answer:

H&M now has over 100 million members.

Explanation:

hope it can help

Answer:

Gross profit margin requires revenue and gross profit of the company.

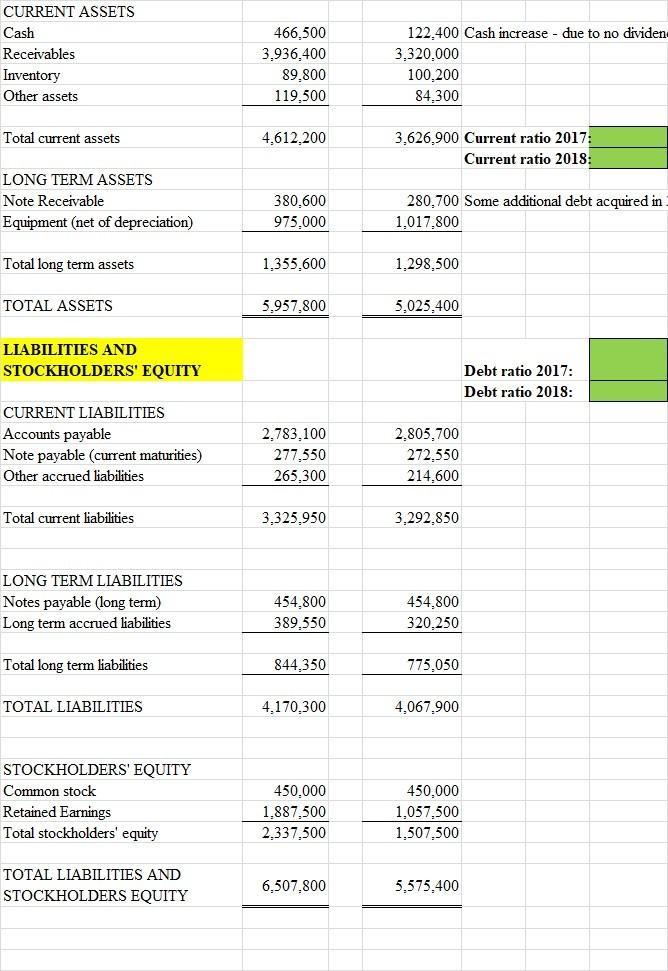

Current ratio = 1.386 x

Debt ratio = 0.123 x

Explanation:

Gross profit margin requires revenue and gross profit of the company which is provided in the question but it can be calculated using this formula ; Total revenue / gross profit . where Gross profit = Revenue - cost of goods sold

Current ratio is calculated using the formula ; current assets/ current liabilities lets assume the left column is for the most recent year then current ratio = 4612200/3325950 = 1.386x

Debt ratio is calculated using the formula ; total debts/total assets lets assume once more that the left column is the most recent year. note; total debts = long term + current notes payable = 454800 + 277550

therefore debt ratio = 732350 / 5957800 = 0.123x

attached is the income statement and balance sheet

All of the above are correct

Answer: True

Explanation: Market segment can be defined as the grouping of a population on the basis of geography, gender or age etc. for the purpose of marketing. The population in every single group has two or more similar characteristics on the basis of which marketing strategy is made.

In the given case, there are two similarities in the group,first the age, and ,second is the hobby of internet.

Hence, it is an example of market segment.

When boating on a river, you might encounter these strainers and the danger of these strainers is that they can possibly trap your boats and throw the passengers out of the boat. Strainer is the term that describes anything that obstructs the way in the river such as logs, or wire fence.