Answer:

c. debits to Cost of Goods Sold during the period

Explanation:

For a Manufacturing firm, the Cost of Sales is equal to the Cost of Goods Manufactured.

Therefore, On the cost of goods manufactured schedule, the cost of goods manufactured agrees with the debits to Cost of Goods Sold during the period.

Answer:

Entries are given

Explanation:

We will record assets and expenses on the debit as they increase during the year and will record liabilities and capital on the credit side as they increase during the year or vice versa.

DEBIT CREDIT

April 01

Account Receivable $3,800

Sales $3,800

Apr - 01

Cost of Goods Sold $2,280

Merchandise $2,280

Apr - 04

Sales Return $460

Account Receivable $460

Apr - 04

Merchandise $276

Cost of Goods Sold $276

Apr - 08

Account Receivable $1,400

Sales $1,400

Apr - 08

Cost of Goods Sold $980

Merchandise $980

Apr - 11

Cash $3,340

Account Receivable $3,340

Answer:

The answer is: D) All of the above

Explanation:

The characteristics of a variable annuity contract are:

- earnings are tax deferred and reinvested

- they offer a Guaranteed minimum death benefit (GMDB)

- depending on the annuity payout option the beneficiary takes, they can provide guaranteed income for life

The beneficiary can decide between different annuity options. Annuity payments can vary depending on the account's earnings.

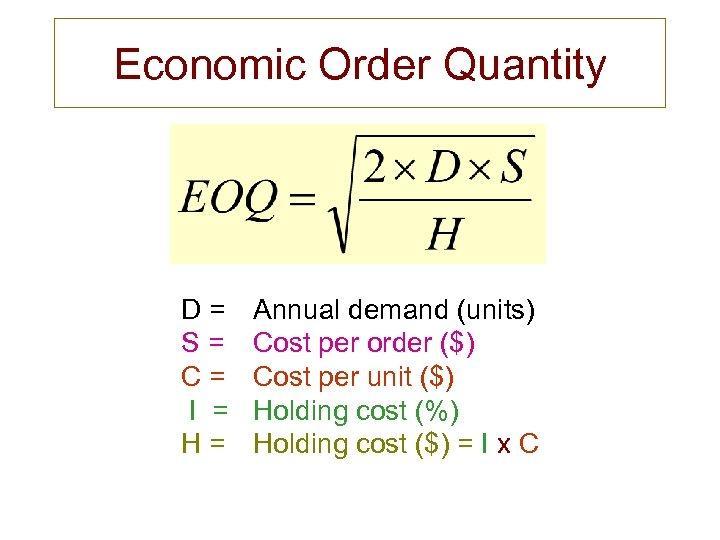

Answer:

The business should order the inventory 25 times per year in a lot of 100 to minimize the inventory costs.

Explanation:

To calculate the lot size that minimizes the inventory cost, we will calculate the economic order quantity (EOQ) which is the order quantity that a business should order in each order to minimize the inventory related costs. The EOQ can be calculated using the attached formula,

EOQ = √[(2 * 2500 * 20) / 10]

EOQ = 100 packages

The lot size for each order should be 100 to minimize the inventory costs.

We can calculate the number of reorders per year by dividing the total annual demand by the EOQ.

Number of orders = 2500 / 100

Number of orders = 25 times

Answer:

Quantity variance.

Explanation:

The difference between actual and standard cost caused by the difference between the actual quantity and the standard quantity is called the Quantity variance.

For instance, if Tony needs a standard quantity of 50 pounds of iron to construct a burglary, but only used 51 pounds, then the quantity variance is 1 pound of iron.

<em>Hence, the quantity variance is simply the difference between the actual quantity of materials that should be used and the quantity of materials that was used. </em>