Many economists believes that WORKERS AND CUSTOMERS BEAR MUCH OF THE BURDEN OF THE COOPERATE INCOME TAX.

Cooperate income tax refers to a direct tax which is imposed by a government on the income or capital of business organisation. Business organisations usually transfer much of this tax burden to their consumers and employers.

Answer: Option (D)

Explanation:

Organic organization is referred to as or known as the type of an informal organization. Organic organization is known as an organization which is known to be very flexible and thus is capable to adapt to the changes. The structure is mostly identified as by having the little to minute job specialization, also there are few layers of the management, the decentralized decision making process.

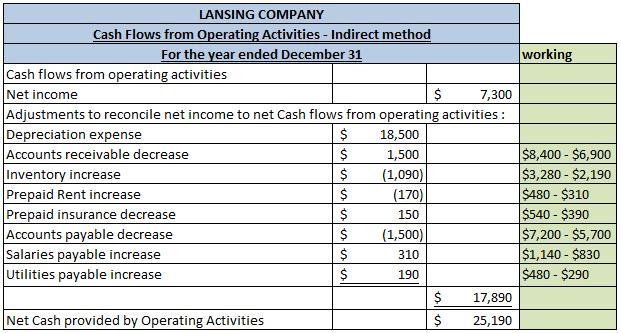

The operating activities generated $25,000 in net cash.

A company's liquidity position is represented by net cash. It is determined by subtracting the current liabilities from the cash balance shown on the financial accounts of the company at the end of a specific period, and analysts and investors use it to gauge the firm's financial and liquidity status.

It differs from net cash flow, which is determined as the cash the company produced during a specific time period after paying all of its operational, financial, and capital obligations, including shareholder dividends.

The company's cash plus marketable investments less its total debt is another way to calculate net cash (short-term borrowings plus long-term borrowings). The company will be able to honor its borrowings if they become immediately due if this figure is positive, which indicates that the company is in good financial condition. If this number is negative, on the other hand, it indicates that the business does not have enough cash on hand to pay off all of its borrowings right away.

Learn more about net cash here

brainly.com/question/12424296

#SPJ4

Answer:

The correct option is lack of personal ethics

Explanation:

Fear of failure could be cogent reason behind employees' resistance to change since most employees would have gotten used to existing arrangement and any attempt to change it might be perceived a leaving one's comfort zone for unknown destination point.

The way individual perceive change can also be a rationale for opposing changes,some employees see changes as an opportunity to record new achievement while some might see as a way to expose their inefficiencies.

Another reason for opposing views to changes could lack of trust, in the sense that management might not keep to their promises made prior to implementing the changes,hence lack personal is the odd option and the correct option.