Answer:

New Long term debt = $8000

Explanation:

The computation of the net new long term debt is given below:

Sales $750000

Less: Expenses:

COGS -$540,000

Selling expenses -$85,000

Depreciation -$190,000

Interest- $65,000

Total Expenses -$880,000

Net Loss -$130,000

Add: Non- cash expense ie. Depreciation +$190,000

Net Cash flow $60,000

Less: Cash Dividend declared -$68,000

New Long term debt = $8000

Answer:

Personalization.

Explanation:

Using personalization in customer relationship management (CRM) requires gathering a lot of information about customers’ preferences and shopping patterns, and some customers get impatient with answering long surveys about their preferences.

This ultimately implies that, personalization deals with gathering information about a specific customer's choice such as taste, requirements, product preferences, shopping styles or patterns in order to be able to serve him or her better, through the provision of goods and services that meets their needs.

I would say B. Quick cash loans. Interest rates are very high & not a good idea in borrowing money. They are designed for people who have poor credit ratings & have no other means to borrow money.

<span>Net gain of $0.40 per headlight.

Let's calculate how much it will cost Peluso to make each headlight.

First, let's add the direct labor and materials costs

$3 + $4 = $7

Now let's add the manufacturing overhead that would actually be affected by making head lights. Since 40% is unaffected, we need to multiply the overhead by 100% - 40% = 60% before attributing that cost to the headlights. So

$6 * 0.60 = $3.60

And let's add that to the current cost of making the headlight

$7 + $3.60 = $10.60

And finally, let's subtract that from the cost of the headlight if outsourced.

$11 - $10.60 = $0.40

So the Peluso company will save $0.40 per headlight that they manufacture themselves.</span>

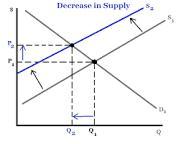

Answer:

Decrease in supply

Explanation:

When a government increases taxes it means that cost of production increases. Suppliers will have no choice but to increase prices at all levels of quantity demanded. This results in a decrease in supply because suppliers will not be able to maintain supply at all price levels.

Supply curve will shift to the left. Find attached an illustration.

If the market for tennis balls was in equilibrium an increase in taxes will result in decrease in ability of supplier to provide the good at all price levels so supply shifts to the left.