Complete question is;

The Internal Revenue Service (IRS) provides a toll-free help line for taxpayers to call in and get answers to questions as they prepare their tax returns. In recent years, the IRS has been inundated with taxpayer calls and has redesigned its phone service as well as posting answers to frequently asked questions on its website (The Cincinnati Enquirer, January 7, 2010). According to a report by a taxpayer advocate, callers using the new system can expect to wait on hold for an unreasonably long time of 14 minutes before being able to talk to an IRS employee. Suppose you select a sample of 50 callers after the new phone service has been implemented; the sample results show a mean waiting time of 12 minutes before an IRS employee comes on line. Based upon data from past years, you decide it is reasonable to assume that the standard deviation of waiting times is 10 minutes. Use a = 0.05.

a. State the hypotheses.

b. What is the p-value (to 4 decimals)?

c. Using a = 0.05, can you conclude that the actual mean waiting time is significantly less than the claim of 14 minutes made by the taxpayer advocate

Answer:

A) Null hypothesis; H0: μ ≥ 14

Alternative hypothesis; Ha: μ < 14

B) P-value ≈ 0.0793

C) The p-value is less than the significance value and thus we will fail to reject the null hypothesis and conclude that the evidence is not sufficient to reject the claim that the actual mean waiting time is significantly less than the claim of 14 minutes made by the taxpayer advocate

Explanation:

We are given;

Population mean time; μ = 14

Sample mean time; x¯ = 12

Population size; n = 50

Standard deviation; σ = 10

A) Let's state the hypotheses;

Null hypothesis; H0: μ ≥ 14

Alternative hypothesis; Ha: μ < 14

B) Let's first find the test statistic from the formula;

z = (x¯ - μ)/(σ/√n)

z = (12 - 14)/(10/√50)

z = -1.41

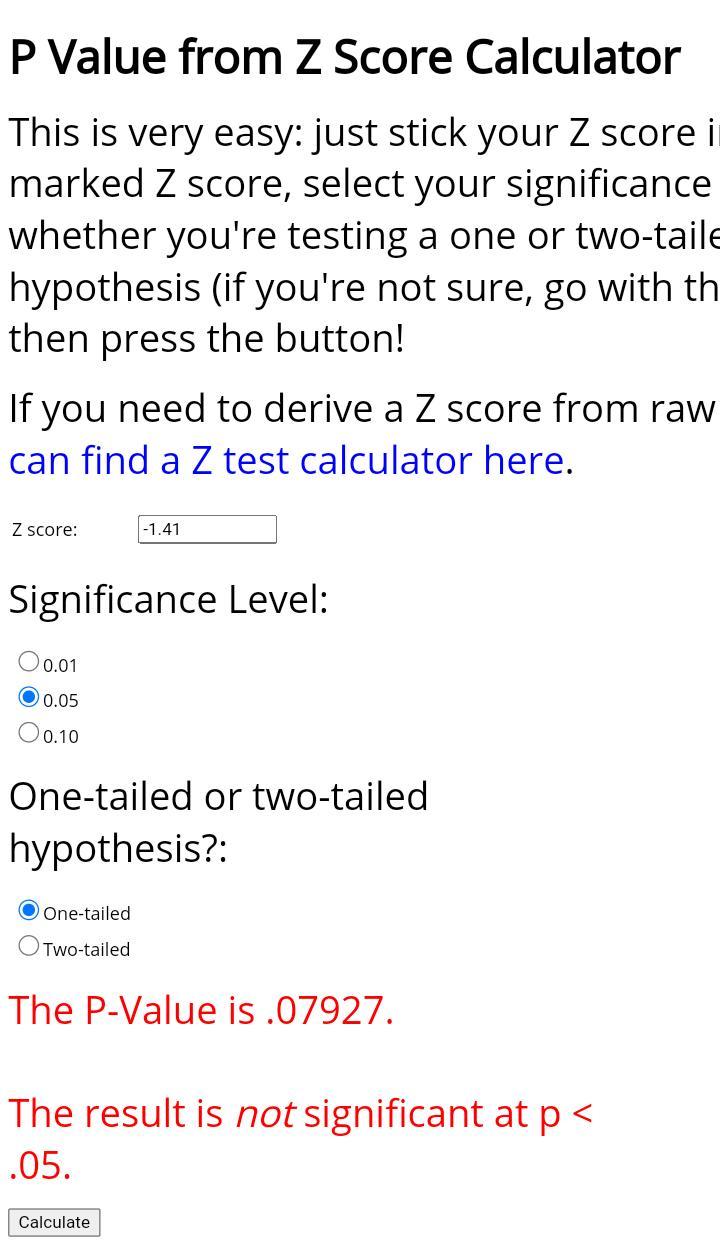

From online p-value from z-score calculator attached using; z = -1.41: α = 0.05 and one tailed hypothesis, we have;

P-value ≈ 0.0793

C) The p-value is less than the significance value and thus we will fail to reject the null hypothesis and conclude that the evidence is not sufficient to reject the claim that the actual mean waiting time is significantly less than the claim of 14 minutes made by the taxpayer advocate