Answer:

(B) False

Explanation:

In fact, if assets have a fixed monetary value, increasing the overall price level (inflation) will reduce the real value of these assets. Thus, the purchasing power of the holders of these assets will decrease. However, it is not correct to say that the holders of these titles have reduced their spending, since what determines spending is individual perceptions and needs. Some of the holders may decrease their spending in the face of an inflationary process, but others may maintain or even increase their spending.

Answer: The correct answer is "Nikkei includes 10% overhead costs and an 8% profit margin in the price of all the parts they export to the U.S.".

Explanation: In her testimony, the president claimed<u> Nikkei includes 10% overhead costs and an 8% profit margin in the price of all the parts they export to the U.S.</u> Using traditional guidelines, Congress determined that Nikkei was not dumping.

It is known as dumping when companies sell products at a lower price abroad than they sell in their country.

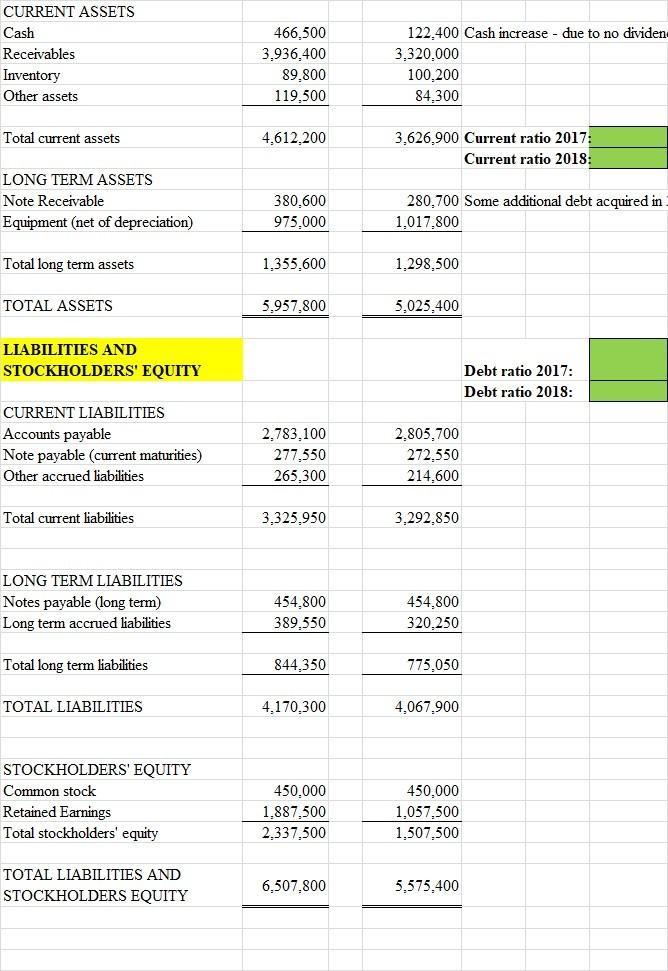

Answer:

Gross profit margin requires revenue and gross profit of the company.

Current ratio = 1.386 x

Debt ratio = 0.123 x

Explanation:

Gross profit margin requires revenue and gross profit of the company which is provided in the question but it can be calculated using this formula ; Total revenue / gross profit . where Gross profit = Revenue - cost of goods sold

Current ratio is calculated using the formula ; current assets/ current liabilities lets assume the left column is for the most recent year then current ratio = 4612200/3325950 = 1.386x

Debt ratio is calculated using the formula ; total debts/total assets lets assume once more that the left column is the most recent year. note; total debts = long term + current notes payable = 454800 + 277550

therefore debt ratio = 732350 / 5957800 = 0.123x

attached is the income statement and balance sheet

A firm's expected revenues and expenses are what should be included in a firm's business model.

<h3>What is a business model?</h3>

A business model is document that contains processes and procedures of how a company would operate.

This document is important for effective organization control and also assist coordinate business relationships amongst stakeholders

Learn more about business model here: brainly.com/question/1171429

#SPJ1

Answer:

Kindly check explanation

Explanation:

Hunger often stems from poverty, Famine, inflation, war and so on. However, factors which often has a direct impact on food and coukd lead to hunger include poverty and Famine. To reduce or forestall this problem on a local and global scale, necessary steps which should be taken are those which tends to address the issue of food security. Which includes the empowerment of farmers and good funding and monitoring of the agricultural sector. Through this food cultivation could be done on a multi dimensional scale by providing support in terms of machinery, low interest loans in otter to enable farmers and other related stakeholders get access to the needs d capital for the development of their agricultural business. Also, good road network for easy transportation of farm produce. Alternative methods of watering such as irrigation farming should be upgraded as this could prove vital during periods of Rainfall shortage. The distribition of foods including adequate regularozation of prices is also key in other to prevent artificial inflation or scarcity in a bid to accrue higher profit.