Answer:

Attached are the detailed solution tables for

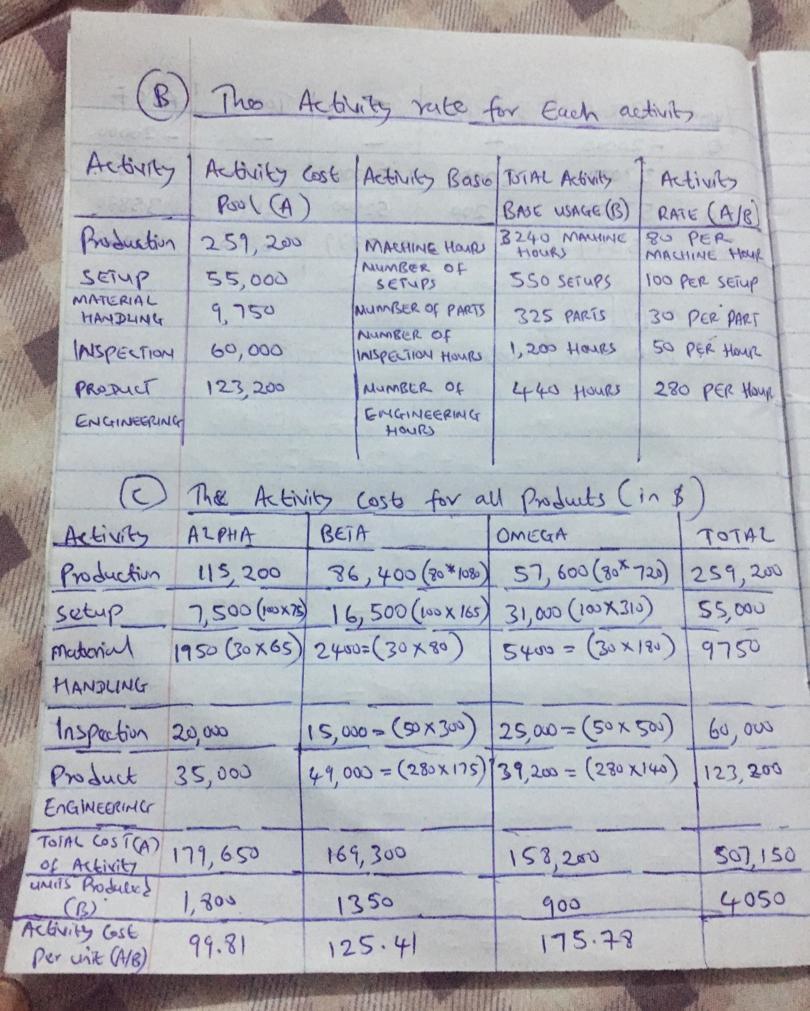

A) complete the activity rate for each activity is a general question covering so solution starts from B

B) calculation of the activity rate for each activity: shown in the attached table

C) activity cost per unit : alpha = $99.81, Beta = $125.41, 0mega = $175.78

D ) The activity unit costs are not equal across all three products because of different activity bases such as machine hours, setups, parts and inspection hours that also determines the activity cost

Explanation:

A) complete the activity rate for each activity is a general question covering so solution starts from (B)

B) calculation of the activity rate for each activity: shown in the attached table

C) Calculation of activity cost of all products

activity cost of each product = use of product activity * activity rate

production = ($80 * Machine hours of each product )

setup = ( $100 * number of setups for each product )

Material handling = ( $30 * number of parts of each product )

Inspection = ( $50 * number of inspection hours for each product )

Product engineering = ( $280 * number of engineering hour for each product )

Activity cost per unit = total cost of activity of each product / unit produced for each product

D) The activity unit costs are not equal across all three products because of different activity bases such as machine hours, setups, parts and inspection hours that also determines the activity cost