Answer:

Explanation:

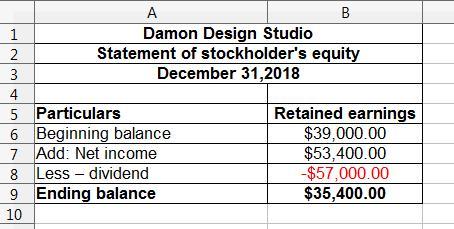

For computing the retained earning ending balance, first, we have to compute the net income. So, the calculation is shown below:

= Service revenue - salaries expense - property tax expense - utilities expense - miscellaneous expense - rent expense

= $154,600 - $65,000 - $2,200 - $7,200 - $3,800 - $23,000

= $53,400

So, the net income would be $53,400

Now, we have to find the ending retained earning balance which equals to

= Beginning retained earning balance + net income - dividend paid

= $39,000 + $53,400 - $57,000

= $35,400

The preparation of the statement of retained earning is presented in the spreadsheet. Kindly find the attachment below: