Answer:

$74.62

Explanation:

Div₀ = $1.09

expected growth $0.19 per year

Div₁ = $1.28

Div₂ = $1.47

Div₃ = $1.66

Div₄ = $1.85

Div₅ = $2.04

then constant growth rte of 5.3%

equity cost = 7.5%

first we need to determine the stock price in year 5 using the Gordon growth model:

stock price = [dividend x (1+g)] / (Re - g) = ($2.04 x 1.053) / (7.5% - 5.3%) = $97.64

now we can discount all the future cash flows:

stock price = $1.28/1.075 + $1.47/1.075² + $1.66/1.075³ + $1.85/1.075⁴ + $2.04/1.075⁵ + $97.64/1.075⁵ = $1.19 + $1.27 + $1.34 + $1.39 + $1.42 + $68.01 = $74.62

Direct real estate investing<span> involves buying a stake in a specific property. For equity</span>investments<span>, this means acquiring an ownership interest in an entity that directly owns an asset such as an apartment community, shopping center or office building. ( from online)</span>

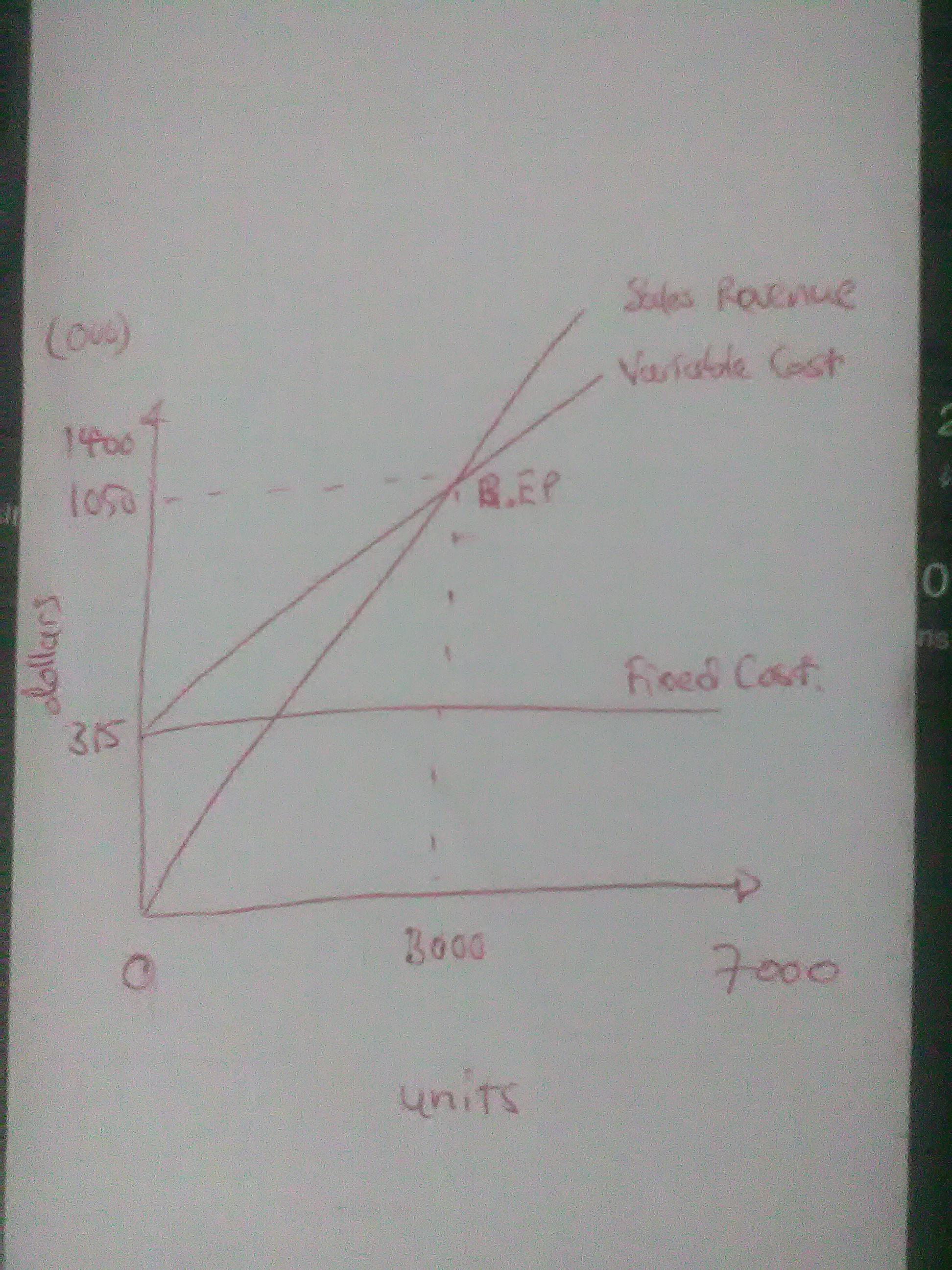

Answer:

1a. 3,000 units

1b. $1,050,000

2. See attachment.

3. contribution margin income statement

Sales ($350 × 7,000 units) $2,450,000

Less Variable Cost ($245 × 7,000 units)) ($1,715,000)

Contribution $735,000

Less Fixed Costs ( $315,000)

Operating Profit $420,000

Explanation:

Break-even point (sales units ) = Fixed Cost ÷ Contribution per unit

= $315,000 ÷ ($350 - $245)

= 3,000

Break-even point (sales dollars) = Fixed Cost ÷ Contribution Margin Ratio

= $315,000 ÷ ($105/$350)

= $1,050,000

Answer:

c. 2.5A^0.36R%0.64/R.

Explanation:

Marginal productivity is the increase in amount of one unit of output with the one unit increase of input. Will can produce higher grade when he studies more hours. His grade will increase by one level when he studies more. His grade production function is the level of increase in his output.

After you've finished the presentation, practice giving it.

<h3><u>Why is it crucial to use effective presentation methods?</u></h3>

Effective presentation methods are crucial because they enable you to convey concepts in a clear, succinct, and engaging manner. A strong public speaking ability enables you to authoritatively present your knowledge and makes you stand out at work. Therefore, in order to portray our best selves whenever we speak in public, we need to identify effective presentation tactics that work for us. Here are the best presentation skills you may learn in light of the many materials available on how to speak in public.

- Maximum one central idea per presentation.

- Do not forget that the audience is on your side.

- Introducing your accent to others tactfully.

- Deliver your idea in terms that your audience can grasp.

- Engage the audience's interest.

- Visualize the data.

- Rather than your presentations, focus on you instead.

- When absolutely required, use technology.

- You should repeatedly practice your presentation.

Learn more about presentations with the help of the given link:

brainly.com/question/13285482

#SPJ4