Answer:

A D F E

Step-by-step explanation:

Answer:8

Step-by-step explanation: Since the opposing way of solving is division, you divide 72 into 9 and you get 8.

Answer:

Brownian Motion- The usual model for the time-evolution of an asset price S(t) is given by the geometric Brownian motion.

Now the geometric Brownian motion is represented by the following stochastic differential equation:

- Note- <em>coefficients μ representing the drift and σ,volatility of the asset, respectively, are both constant in this model.</em>

To solve the problem now we have the been Data provided:

μ= 0.12,

σ=0.24,

Step-by-step explanation:

<u>Step A:</u>

we have, the variables of Black Scholes Model, by putting the values of variables available, we get:

- S = Current stock price = 40

,

Next is, "r" the risk free rate,

- risk free rate, r = mu = 0.12

,

- time to maturity, T, as we have;

- T= 4 months = 4/12.

- T = 1/3 year(360 days)

<u>Step B:</u>

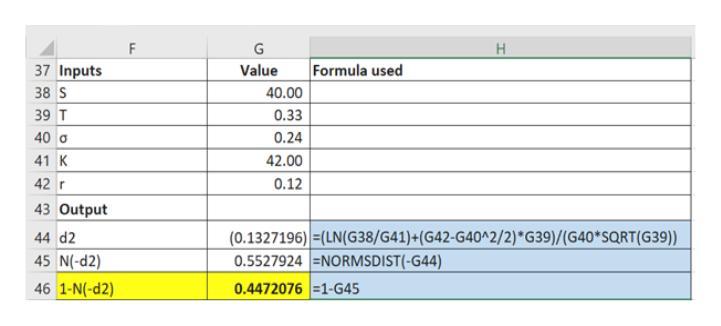

We now need to calculate the parameter d₂ of the Black Scholes Model. .

- The probability which we want is 1 - N(-d₂),

<u>Step C:</u>

As step C is done on excel for further calculations so, do use it if you are solving it on computer.

Well from positive y axis Q is situated at 6 units while P is situated at 3 units.

So length of PQ - 6+3 = 9 units.

Rounding up your answer is 10 units