Answer:

0.066 cent

Explanation:

Efficiency (E) = Energy output (Eo)/Energy input (Ei)

Eo = E × Ei

E = 0.6

Ei = mass × acceleration due to gravity × height

mass = 100lbm = 100×0.45359kg = 45.359kg, height = 300ft = 300/3.2808 = 91.44m

Ei = 45.359×9.8×91.44 = 40646.7Ws = 40.6467kWs = 40.6467kWs × 1h/3600s = 0.011kWh

Eo = 0.6 × 0.011kWh = 0.0066kWh

1kWh = 10 cents

0.0066kWh = 0.0066×10 = 0.066 cent

Answer:

8.3 times

43.8 days

Explanation:

Accounts receivable turnover measure the average times the company received their receivable, It measure the efficiency of the company regarding collection from customers. Turnover will be higher if company has low ratio of receivables to sales value.

Average Receivable can be calculated as below

Average Receivable = (Accounts Receivable at the beginning of the year + Accounts Receivable at the end of the year) / 2 = ($50,000 + $70,000)/2 = $60,000

Net Sales = $500,000

Formula for Accounts receivable turnover is as follow

Accounts receivable turnover = Net Sales / Average Receivable

Accounts receivable turnover = $500,000 / $60,000 = 8.3 times

Days Sales Receivable is also know as Days receivables. It is an method of estimation of a company for the receivables value. it measure the numbers of days at average account receivable take after sales to convert into cash.

Formula for Days Sales Receivable is as follow

Days Sales Receivable = ( $60,000 / $500,000 ) x 365 = 43.8 days

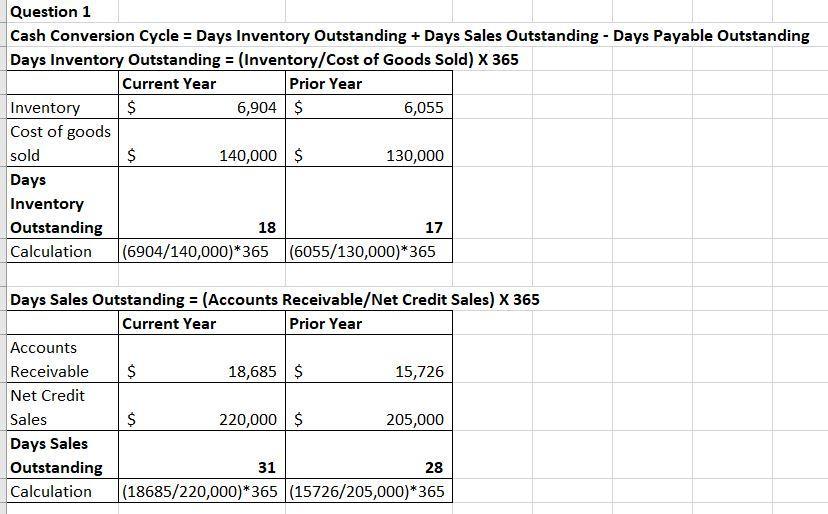

<em>Find the given attachments for the complete solution</em>

<em />

Answer:

provide a uniform response to all hazards that a community may face.

Explanation:

Emergency Operation plan is referred to that document which focus on response given to particular emergency. it direct guideline which focus planning for any disaster in efficient and effective way.

It include six element on which this plan work. some of them are listed below:

1- communication

2 -resources and assets

3- safety and security

4 - staff responsibilities

5 -utilities

6 -clinical support

A high Deductible Plan will get you the least out of pocket expenses