Answer:

Marketing Mix

Explanation:

According to my research on the strategic marketing planning process, I can say that based on the information provided within the question Molly is engaged in the Marketing Mix step of this process. This step focuses on Product Development, Pricing, Promotion, and Distribution. Which the ones in bold are what Molly is doing.

I hope this answered your question. If you have any more questions feel free to ask away at Brainly.

Answer:

From all indications,it is very clear that the question requires a journal entry to record the unpaid interest.

Dr Interest expense $1125

Cr Interest payable $1125

Explanation:

This is a typical case of an omitted entry in the books of accounts,specifically it relates year-end close accounting adjustments.

Under the accrual basis, which is prevalent in the private sector,expenses are to recorded when incurred not when they are settled in cash,as result it is imperative that the above transaction needs be adjusted by debiting interest expense account and crediting same amount to interest payable account to affirm that the company has an obligation to $1125 to mortgage providers.

The statement “Expenses, such as depreciation on buildings

are also known as variable expenses.”, is false, due to the fact that depreciation

is a fixed cost since throughout its useful life as an asset, it reoccurs in

the same amount per period, and thus, depreciation cannot be considered a

variable cost. Nevertheless, as with all things, there is an exception. The

depreciation will be sustained in a pattern that is more consistent with a

variable expense, only if a business recruits a usage-based depreciation methodology.

To add, the corporate expense that alters with the company’s

production output is called the variable cost.

Answer: <em>It focuses on overall firm performance, providing a more aggregated viewpoint.</em>

Explanation:

Financial accounting can be referred to as a specialized arm of accounting which keeps record of an organization's financial transactions. It tends to use standardized guidelines under which transactions are recorded, stated, summarized, and thus presented in a financial report or statement i.e. an income statement, balance sheet etc.

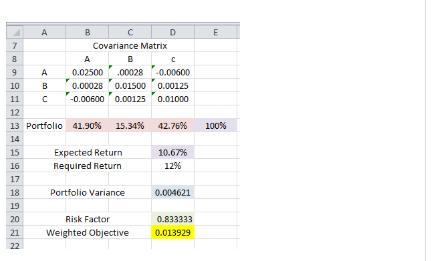

Answer:

If minimizing the risk is important according to the solver report the way of investing is A=41.9% ,B=15.34% and C =42.76%

Explanation:

Please see attachment