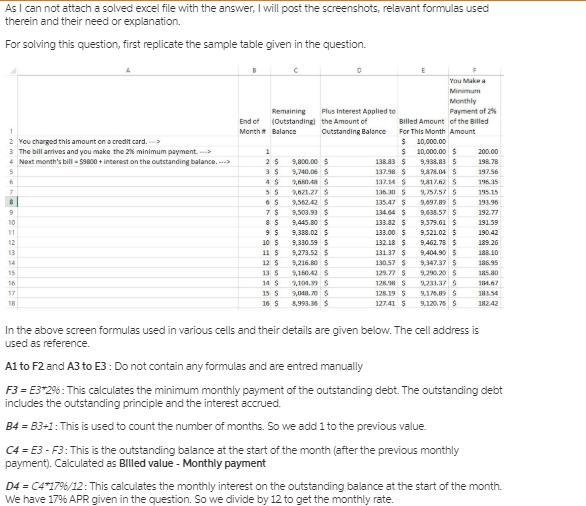

Answer:

B. conformity

Explanation:

Conformity is a term in psychology that describes the tendency of a person(s) to adopt the behaviour of the people around them or of the people in a group they belong to.

Monica adopted the behaviour of her group of friends.

Labelling theory postulates that individuals may adopt the characteristics of the labels people use to describe them and this may shape their identity.

Differential association theory states that people learn how to become criminals by interacting with people.

The answer would be C. Webcam, Speakers, and microphone.

D. Because he is listening to her fully and making sure he fully understands what she is asking

Answer:

c. attention is paid to competitive priorities and strategic fit.

Explanation:

Managing process is the top level activity it involves various activity and decisions for the growth of an organization. It clearly states that the company shall grow, what are the goals, what are the objectives and what are the strategies.

This clearly reflects that management's main concern is to strategic performance, and how does it create a space in the market share, as gaining from competitive advantage.