Answer:

B) will; less than

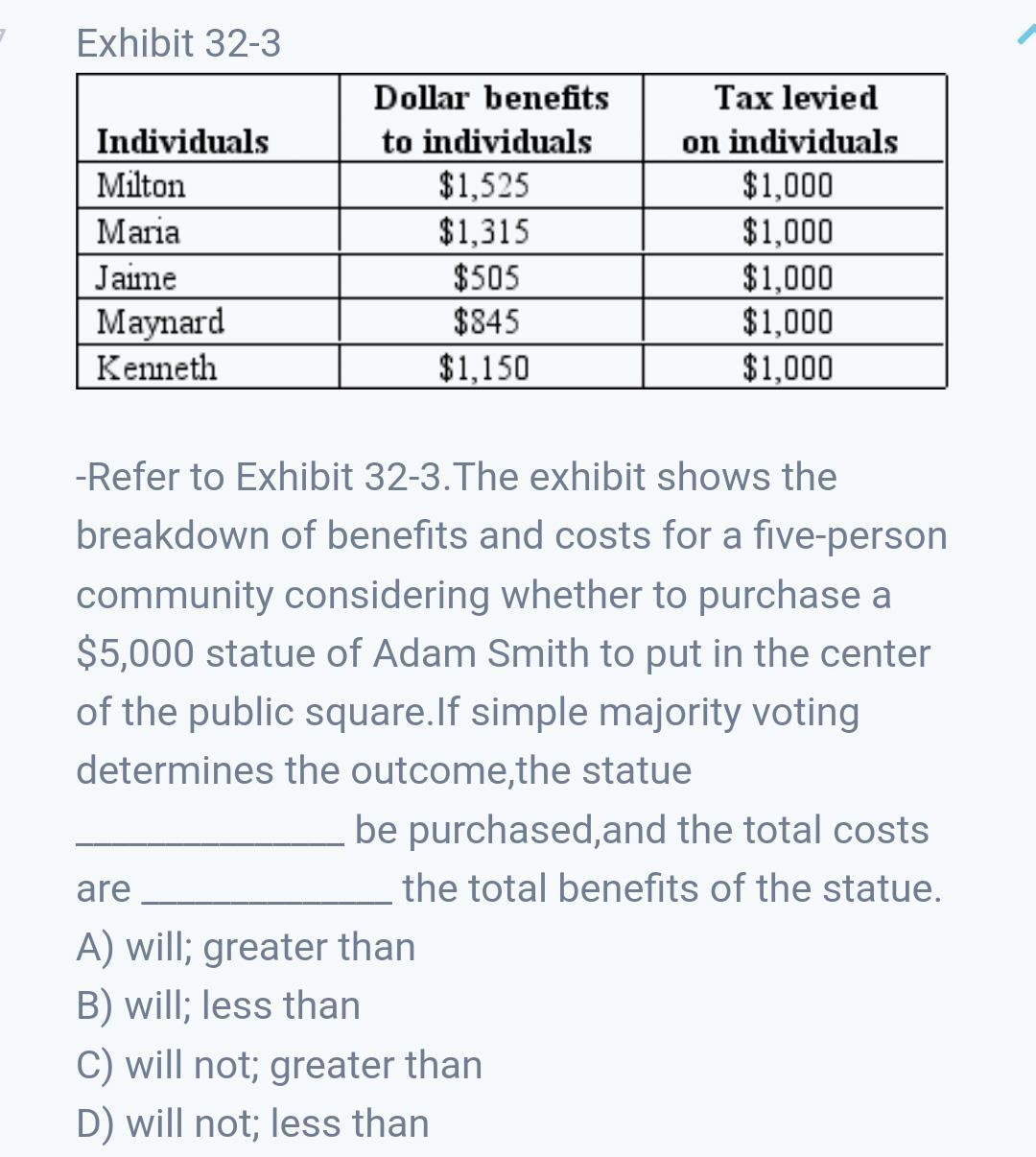

The exhibit shows the breakdown of benefits and costs for a five-person community considering whether to purchase a $5,000 statue of Adam Smith to put in the center of the public square. If simple majority voting determines the outcome, the statue will be purchased, and the total costs are less than the total benefits of the statue.

Explanation:

Attached is the completed question, including the table used for this question;

From the table;

For Milton, Maria and Kenneth the benefits of the statue is more than the cost levied on them(they would be in support)

For Jaime and maynard the benefits of the statue is less than the cost levied on them (not in support)

Since majority voting will determine the outcome, the statue will be purchased (3 in support and 2 against, majority is in support)

Total cost = $5000

Total benefits = $(1525+1315+505+845+1150) = $5340

Therefore, the total cost is less than the total benefits

Answer:

RAM devices are typical read/write memories

Explanation:

read/write memory A type of memory that, in normal operation, allows the user to access (read from) or alter (write to) individual storage locations within the device.

Answer:

a bigger space

Explanation:

a bigger space because u have a alot to do. you can have more people working. or if it private then a room for secretary and your office in the business

Answer:

The first investment is more profitable than the general market interest rate.

Explanation:

Giving the following information:

An investment will pay $202,000 at the end of next year for an investment of $182,000 at the start of the year. The market interest rate is 7.9% over the same period.

<u>To compare both options, we need to calculate the final value of investing the $182,000 in other investment that pays a 7.9% interest rate.</u>

We need to use the following formula:

FV= PV*(1+i)^n

FV= 182,000*(1.079)= $196,378

The first investment is more profitable than the general market interest rate.

Answer:

Given:

Implicit Cost = $65,000

Total revenue = $150,000

Explicit cost = $85,000

Here, we'll compute the economic profit for the first year as :

<em>Economic profit = Total revenue - (Explicit cost + Implicit Cost)</em>

<em>Economic profit = </em>$150,000 - ($85,000 + $65,000)

<em>Economic profit = $0 </em>

<em></em>

<em>∴ </em><u><em>Tom’s economic profit for his first year in business will be $0</em></u>

<u><em>The correct option is (a).</em></u>