You can give numerical ratings to possible career choices to help determine if they are right for you by creating a(n) personal career profile.

Answer:

Correct option is (A)

Explanation:

Companies that are price setters or price makers produce unique products as they have an advantage over others. They are price makers as they enjoy monopoly in the market.

Companies producing homogeneous products cannot be price setters as there are many other companies operating in the same market so prices are set by the market forces.

Answer:

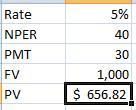

$656.82

Explanation:

The calculation of required return is shown below:-

Face value (FV) = $1,000

Coupon rate = 12.00%

Number of compounding periods per year = 4

Interest per period (PMT) = $1,000 × 12.00 ÷ 4

= $30.00

Number of years to maturity = 10

Number of compounding periods till maturity (NPER) = Number of compounding periods per year × Number of years to maturity

= 40

Required rate of return = 20.00%

Required rate of return per period (RATE) = 5.00%

Bonds value = -PV(RATE,NPER,PMT,FV)

= $656.82

Therefore we applied this formula into excel.

Answer:

0.99

Explanation:

Elasticity is an economic metric that looks into the proportional change of an economic variable in response to a change in another. Therefore, elasticity of supply refers to the ratio of the proportionate change in the quantity supplied to the proportionate change in price. A higher value of elasticity implies supply sensitivity to price changes. The converse is also true.

Given,

Equilibrium price, ![E_{p} = [tex]P_{1}](https://tex.z-dn.net/?f=E_%7Bp%7D%20%3D%20%5Btex%5DP_%7B1%7D) =2.50[/tex]

=2.50[/tex]

Equilibrium quantity, ![E_{q} = [tex]Q_{1}](https://tex.z-dn.net/?f=E_%7Bq%7D%20%3D%20%5Btex%5DQ_%7B1%7D) =25.0[/tex]

=25.0[/tex]

At price 10.75=

Quantity supplied of pancakes,  =105.0

=105.0

Elasticity of supply of pancakes,

=

The elasticity of supply for pancake is 0.99

Answer:

The correct answer is C. Stand-alone branding.

Explanation:

In the model of independent brands (house of brands) different brands coexist independently acting on the basis of the different lines of business. This model allows attacking different market segments with specialist brands in each of them, but in the face of the great freedom it provides, minimal synergies between brands are used. For example, LVMH, the world leader in luxury products, has in its portfolio brands such as MOËT & CHANDON, DIOR, AG HEUER or SEPHORA, among others, which operate without any link to the corporate brand.