Answer:

75 percent

Explanation:

The good roads amendment is a law enacted by legislatives in the USA states that ensure maintenance of roads in each state as well as interconnecting roads.

It states, amist other things, that 75% of road user fees collected through tolls and other means are spent on road maintenance.

Cheers.

Answer:

$43,000

Explanation:

Implicit cost or opportunity cost is the cost of the next best option forgone when one alternative is chosen over other alternatives

by starting his business, he forgoes the opportunity to earn 43k

<span>You will find every escrow entry showing the running balance after each receipt or disbursement in a journal kept by the sponsoring broker. This journal must show the chronological order of the transactions when funds are received or disbursed by the sponsoring broker.</span>

Answer:

Structural

Explanation:

It is correct to say that Tina's scenario is an example of structural unemployment, that there are structural economic changes, which can have several different reasons, in the case of the above question, the structural change was caused by a technological change that made the newspaper where Tina worked if she scanned, and Tina's skills were not sufficient to keep up with such changes, which resulted in her resignation.

This is a type of long-term unemployment, which can negatively impact a society, with a large number of people unemployed and disqualified for current job openings, to reduce this problem, it is necessary that companies invest in training programs and effective qualifications so that its employees can follow the structural changes that occurred in their jobs.

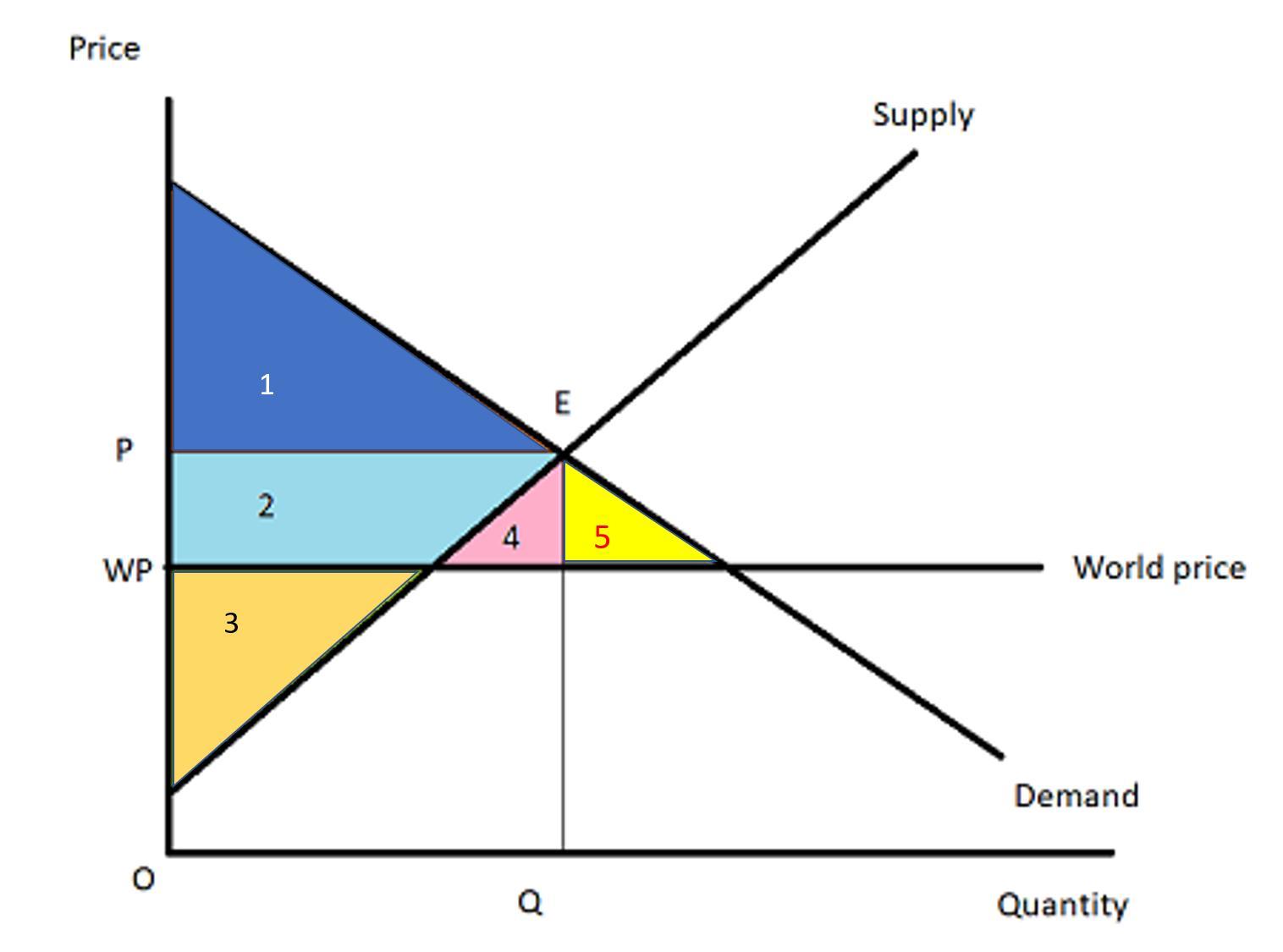

A) As indicated in the illustration, the world price is below the equilibrium level (WP) in free trade. In Canada, the cost is P. The economy's surplus is as follows:

- (1+2+4+5) represents the region of consumer excess.

- The area is represented by producer surplus (4).

- The total excess is represented by (1+2+3+4+5).

b) The devastation of the grape crop in the Gulf Stream will cause an economic supply shock. This will restrict grape supply, causing grape prices to rise owing to a lack of supply. This will raise wine prices all around the world. As a result, as illustrated in the graphic, the global price of wine will now rise. The Canadian wine price will be P, while the global wine price will be WP.

The economy's surplus is as follows:

- The area is represented by consumer excess (1).

- (2+3+4) represents the region of producer surplus.

- The total excess is represented by (1+2+3+4).

<h3>What is Equilibrium Level in Economics?</h3>

When aggregate supply and aggregate demand are equal, an economy is said to be at its equilibrium level of income. In other terms, it occurs when GDP equals total spending.

When supply and demand levels align, economic market equilibrium occurs, resulting in perfect market circumstances for buyers and sellers. Microeconomic and macroeconomic equilibrium are two forms of economic equilibrium. Supply and demand between buyers and sellers are balanced in microeconomics.

Learn more about Equiblibium Level:

brainly.com/question/14202392

#SPJ1