Answer:

Bribery

Explanation:

Bribery is an act of influencing someone's behavior to obtain an undue advantage through giving or receiving unearned rewards .It can be in the form of gifts , money , preferred treatment , and other form of favor , but what actually defines a bribe is the intention behind the gifts.

It has a lot of negative effects either directly or indirectly on the public as it undermines equity , efficiency , integrity in the public service , undercut public confidence in markets , adds to transaction cost and effects the safety and well being of the general public .

The Stock A is the riskiest of all the available stock.

Explanation:

Risk perception of the stock is a very important component of the investment industry.

Standard deviation is the most common parameter to evaluate the risk parameter of any stock. It helps an investor in assessing the volatility of the stock and market.

Higher the price more is the volatility and higher would be a standard deviation. A lower price would eventually translate into low standard deviation.

However, it is to be remembered that the standard deviation is not the only measure of risk perception of the stock.

Answer:

no

Explanation:

honestly the only difference typically these days between senior and average is time spent at company. However, this does not make the average worker less or worse than the senior, and they could be even better. Therefore, the pay should be according to the rank that the person is, not senior wise, but profit wise.

Answer:

Year 1= 1.5%

Year 5= 3.5%

Year 10= 3.5%

10 year nominal interest rate will be 3.5%

Explanation:

Answer:

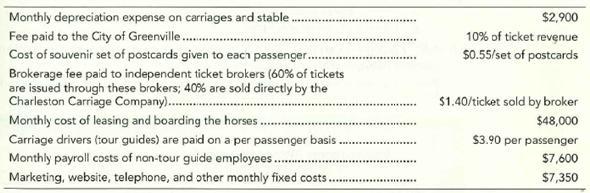

1) Colt Carriage Company

Income Statement

For the month ended April 202x

Revenues:

- Adults passengers $186,300

- Children $81,000

- Total revenues $267,300

Variable costs:

- City fees $26,730

- Souvenirs $7,425

- Brokerage fees $11,340

- Carriage drivers $52,650

- Total variable costs <u>$98,145</u>

Contribution margin $169,155

Period costs:

- Depreciation $2,900

- Horse leases $48,000

- Marketing expenses $7,350

- Payroll expenses $7,600

- Total period costs <u>$65,850</u>

Operating profit $103,305

2) If the total amount of passengers increase by 10%, then all variable costs will increase by 10% except brokerage fees which would increase only by 6%. Revenues should also increase by 10%. Period costs should not change.

Contribution margin should increase by 10.29% and operating profit would increase by 16.81%.

Explanation:

since the information is not complete, I looked it up:

Revenues

13,500 passengers:

8,100 x $23 = $186,300

5,400 x $15 = $81,000

total $267,300

variable costs:

fees paid to the city 10% of total revenue

souvenirs $0.55 per passenger

brokerage fees 60% of total tickets x $1.40

carriage drivers $3.90 per passenger

fixed costs:

depreciation $2,900

horse leases $48,000

marketing expenses $7,350

payroll expenses $7,600