Answer:

Explanation:

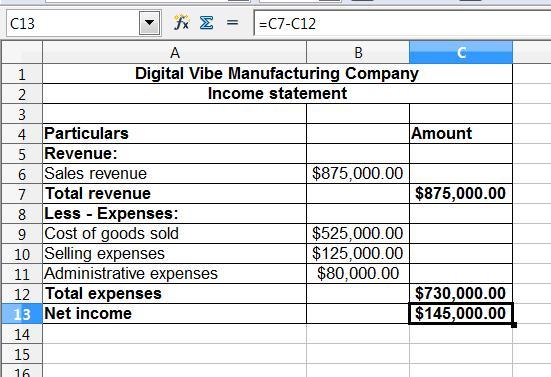

a. In the income statement, the total revenues and the total expenses are recorded.

If the total revenues are more than the total expenditure then the company earns net income

And, If the total revenues are less than the total expenditure then the company have a net loss

This net income or net loss would reflect in the statement of the retained earning account.

Before preparing the income statement, first, we have to compute the net loss or net income which is shown below:

= Sales - cost of good sold - selling expenses - administrative expenses

= $875,000 - $525,000 - $125,000 - $80,000

= $145,000

b. The computation of the inventory balances are shown below:

Direct material = Purchased material - used material

= $168,500 - $149,250

= $19,250

Work in progress = Used material + direct labor wages + factory overhead - transferred units

= $149,250 + $360,000 + $120,000 - $600,000

= $29,250

Finished goods = Transferred units - cost of goods sold

= $600,000 - $525,000

= $75,000

The preparation of the income statement is presented in the spreadsheet. Kindly find the attachment below: