Marx would maintain that Sally has experienced <u>false class consciousness</u>.

<u>Explanation</u>:

False class consciousness is the term used to describe the behavior of the employees who identify themselves as investors by mistake when they own few shares of stock or work as managers in large corporations. This term false class consciousness was used by famous sociologist Karl Marx.

In the above scenario, Sally was working for Ellis Corporation as a computer programmer. But she thinks herself as a stockholder as she holds few shares of Ellis stock and had $15,000 in her savings account.

Answer:

First 4 subparts are answered below:

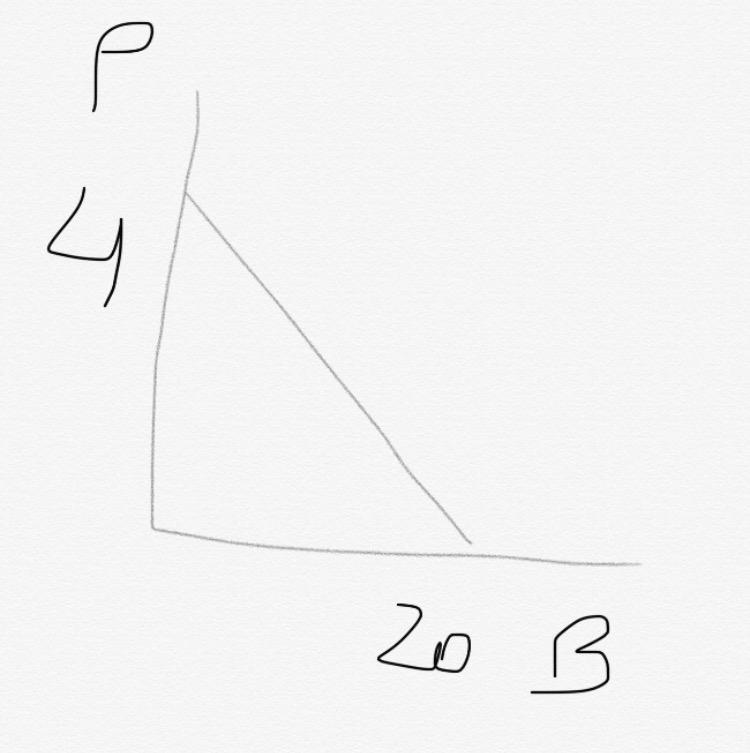

A)

Equation for budget constraint: p1.x1 + p2.x2 = M

Substituting the given information gives: 1B + 5P = 20

B)

The budget constraint is below: See attachment

C)

Slope of budget constraint: -P(pizza)/P(beer) = -5

D)

New budget constraint: 2B + 5P = 20

New slope: -5/2 = -2.5

New constraint line: See attachment

I would go with C. Approach the Federal Trade Commission

Answer:

The high road of this part of the bible defines cooperation and continuity in the work setting with ethical behavior.

Explanation:

Beyond just the work environment, value pairs are applied to day-to-day decision-making and to encounters with both the refer squad. It's also a core competency for maintaining the manager 's reputation.

Next, a bit of comparison and context. Morality is not morality. Ethics is a very unique, independently held code of conduct. Morality has a fluidity that varies over time, depending on social and cultural norms. Imagine the reaction to Brittney Spears for a minute when she appeared in the 1960s on Ed Sullivan show.

Answer:

The correct answer is letter "E": If many firms can supply an input comma then suppliers are unlikely to have the bargaining power to limit a firm's profits.

Explanation:

The negotiating power of suppliers determines the level of competition in a market, according to the concept of the <em>five competitive forces</em>. If only a few companies can supply output or if the input is limited, suppliers are likely to have the bargaining power to limit the income of a business.