Answer: a)The decision tree is attached as a document to this question.

b)$140000

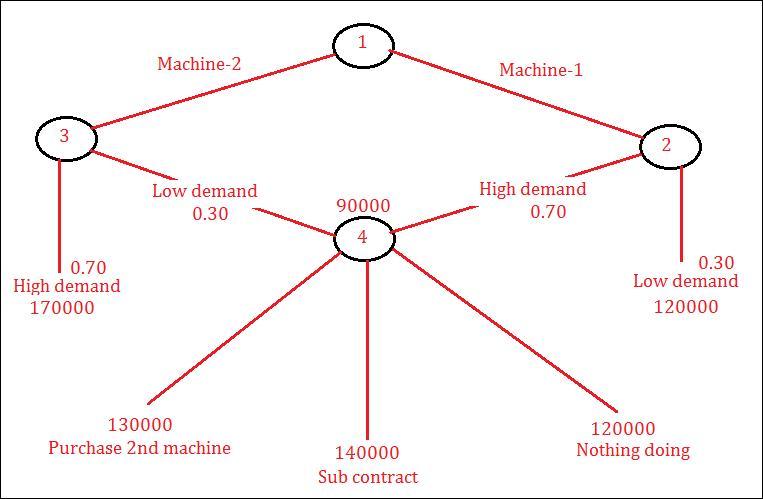

Here is the complete question:

. A manager is trying to decide whether to buy one machine or two. If only one is purchased and demand proves to be excessive, the second machine can be purchased later. Some sales will be lost, however, because the lead time for purchasing this type of machine is 6 months. In addition, the cost per machine will be lower if both are purchased at the same time. The probability of low demand is estimated to be 0.20. The after-tax net present value of the benefits from purchasing the two machines together is $90,000 if demand is low and $180,000 if demand is high.

If one machine is purchased and demand is low, the net present value is $120,000. If demand is high, the manager has three options. Doing nothing has a net present value of $120,000; subcontracting, $160,000; and buying the second machines, $140,000.

a. Draw the decision tree for this problem.

b. Use the decision tree to determine how many machines the company should buy initially and give the expected payoff for this alternative.

Explanation:

Concepts and reason

The expected value of perfect information (EVPI)= EPPI - EP

(EPPI) =expected payoff with perfect information

(EP)= maximum expected payoff computed under uncertainty.

Fundamentals

The expected payoff = P₁X₁ + P₂X₂ +....PnXn,

The formula for the expected payoff is, E(X) = ΣxΡ(x)

Suppose you have a set of corresponding probabilities for playing your pure strategies = Pn

where the probabilities must all be greater than or equal to zero and they all sum to one.

b) the values at node 4 = $120000, $140000 and $160000

EV =maximum(node4)

=max($120000, $140000 , $160000)

=$140000

expected payoff at node 4 = $140000