They've either had crippling addictions, lacked the will to work, disabled, or just went bank rupt from a bad deal.

Answer:

C. middle of the road management

Explanation:

Leadership grid refers to a situation when a leader put too much emphasize on one part of the operation while neglecting the others. In the end, this will reduce the overall's productivity.

Example of leadership Grid:

When managers force the employees to work overly long hours every day because they believe it will bring more profit for the company. But in the end, the employees felt a burn out and many of them eventually quit or become too tired to be fully productive.

To handle leaderships grid, middle of the road management tend to be preferred.

The reason for this is that middle of the road management tend to implement balanced concern between the business and the people who work in it. This management will create a schedule that allow the employees to fulfill the needs in their personal life and career. In the long run, this will create a positive environment in the workplace and improve the productivity as a whole.

Answer:

173,333.33

Explanation:

Lumpsum + Appraisal = Total Spent

500,000 + 20,000 = 520,000

Land + Building + Equipment = Total Fair Value

100,000 + 200,000 + 300,000 = 600,000

Building Costs:

Fair Value Building / Total Fair Value = % of the building cost to apply to the total spent x Total Spent

200,000 /600,000 = .3333 x 520,000 = 173,3333.33

Answer:

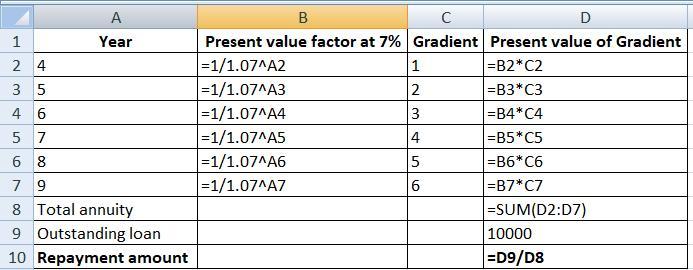

$778.05625

Explanation:

The computation of the amount of repayment is shown in the attachment below:

Given that

Proceeds for year 4 through 9 at $2Z, $3Z

The Principal of the loan amount = $10,000

Interest rate = 7% per year

Based on the given information, the value of Z or the amount of repayment is

= Principal of the loan amount ÷ Total annuity

= $10,000 ÷ 12.85254119

= $778.05625

The answer is a corporation.

A corporation is the most complex business type to establish. While a sole proprietor can open up a business nearly instantly, a corporation has to go through a legal process which includes things like establishing the corporation, selling stock, and establishing a board of directors.