Answer:

sales forecasting

Explanation:

Sales forecasting is a mathematical tool or process to estimate the amount of sales for a product over a given period of time.

Sales forecasts helps companies to make better business decisions so as to analyse the short-term and long-term performance.

The basis for the forecast are generally the past sales data of the product, industry-wide comparisons, and the economic trends for the related products.

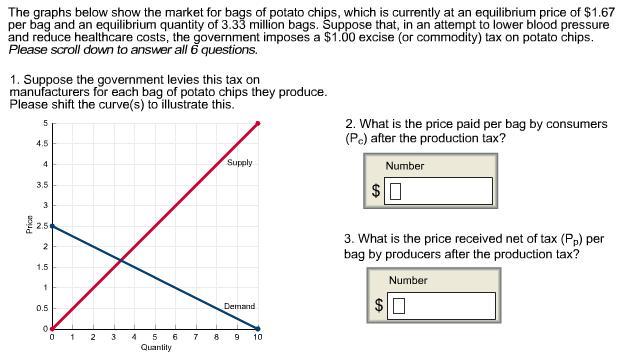

Answer:

Equilibrium is the point of the interaction between the demand and supply curves.

The given graph given from the question is attached below (Image 1-2)

The solution is attached in image 3-4

Answer:

Customer relationship management

Explanation:

- Customer relationship management is also known as (CRM)

- Customer relationship management has a great role in building interaction between the companies and customers

- It is more based on the strategies and technology rather than meeting individually.

- Social media plays a great role in customer relationship management.

- It is the best way to attracts the customer towards the product.

Answer: True

Explanation:

Project plan execution is the second step in Project Integration Management, after Project plan development.

Directing and managing project work involves carrying out the all activities included in the Project plan development.

However, when carrying out the project plan, various sections or elements of the projects should be optimally coordinated according to the strategy and activities established in the master plan.