Answer:

15%

Explanation:

The maximum rate of return that would be paid to borrow an additional $4,000 needed can be calculated as

Rate of return = $600/$4000

Rate of return = 0.15 or 15%

NOTE: The amount of interest is the difference of interest earned at higher yield and interest earned at a lower yield.

Interest earned (higher yield) = $10,000 x 8%

Interest earned (higher yield) = $800

Interest earned (lower yield) = $14,000 x 10%

Interest earned (lower yield) = $1,400

Difference = $1,400-$800

Difference = $600

Answer:

Answer for the question:

Assume that the hypothetical economy of Molpol has 8 workers in year 1, each working 1,200 hours per year (40 weeks at 30 hours per week). The total input of labor is 9,600 hours. Productivity (average real output per hour of work) is $10 per worker

Instructions: In parts a and b, round your answers to the nearest whole number. In part c, round your answer to 2 decimal places.

a. What is real GDP in Molpol? Suppose work hours rise by 2 percent to 9,792 hours per year and labor productivity rises by 5 percent to $10.5

b. In year 2, what will be Molpol's real GDP?

c. Between year 1 and year 2, what will be Molpol's rate of economic growth? percent

Is given in the attachment.

Explanation:

Answer:

The correct answer is c. If an employer wants the employee to work more hours in a week, the result is a larger paycheck.

Explanation:

The salaried worker gives his workforce to another person, who pays him a salary in exchange. It can be said that an employee is an employee of a company or entity, unlike independent or autonomous workers.

Being a salaried worker means having to respect a series of rules and face duties such as meeting the established schedules, respecting their peers and superiors, performing the tasks they have been assigned.

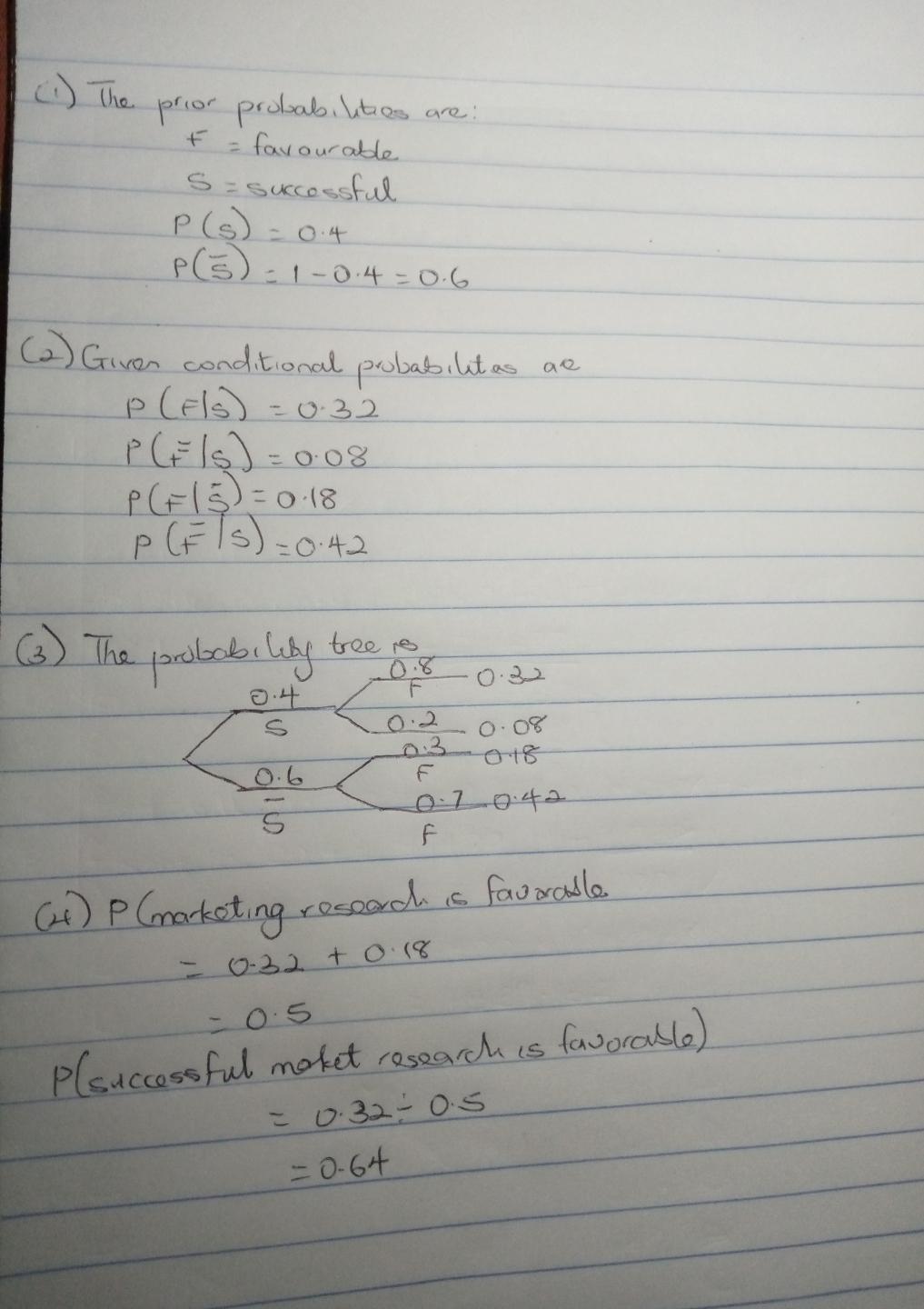

Answer: The answer is attached

Explanation:

Probability is the likelihood or the chance of an occurrence of an event happening. Probability is the number of ways to achieve success in a total number of possible outcomes.

The calculation for the above question is attached

Answer:

We feel that the big data approach is applicable for all three of Gap Inc.’s brands, although the biggest insights from the information collected will come from the brand that has the greatest product diversity. Banana Republic is Gap’s most targeted brand with its expensive price points, so designers already have a relatively good idea of what their customers are looking for. The target customer is upscale, predominantly female, and interested in a classic look. The variability in design for the brand is least among Gap’s, but still significant so the ability to assess the success

of product offerings in real time is extremely valuable. Similar to the model used by Netflix, withonline shopping Gap does not have to rely on feedback from just the very few customers that choose to comment on and rate products that they purchase.With the introduction of “Product 3.0”, the trends seen at Banana Republic and the Gap were able to cascade down into the less expensive, family brand of Old Navy. This allowed for consumers of all income brackets to be touched. All brands had a clear vision with common ground, being more predictive and demand driven based on data analytics. This sharing of information benefits all of the brands by better streamlining products towards market trends. Since Old Navy and Gap have a greater number of SKU’s, they will have an even greater benefit from big data. But managing, purchasing and inventories for these companies is even more challenging, and having to deeply discount unsuccessful SKU’s can be unavoidable. But minimizing these unsuccessful products can be achieved through big data by analyzing how well a product performs before waiting to receive customer feedback. Gap can emulate fast fashion companies like Zara who keep production runs short, even shorter for unsuccessful runs, and create a sense of urgency from the customer without complicating the customer’s decision process with an inevitable sale

Explanation: