Answer:

$320,000

Explanation:

EBIT is earnings before interest and tax.

This case in point ignores the financing impact of interest expense, EBIT is the same as the net income plus taxes

net profit margin=net income/sales

net profit margin=10%

net income is unknown

sales=$3,000,000

10%=net income/$3,000,000

net income=10%*$3,000,000=$300,000

taxes=$20,000

EBIT=$300,000+$20,000=$320,000

Answer:

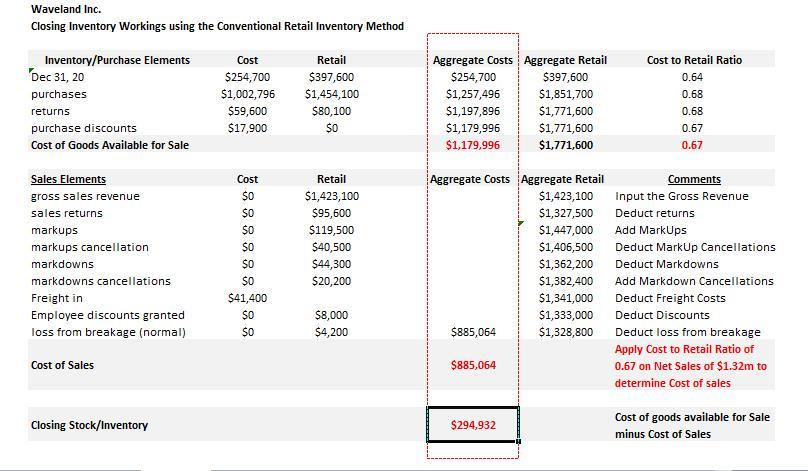

Closing inventory is $294,932

Explanation:

The retail inventory method is used by retailers in estimating their closing inventory.

It identifies the relationship between cost and retail prices and thus associates cost to its net sales using the cost to retail ratio to work our its costs of sales which further guides in defining what his profit ought to be.

The cost to retail ratio is cost price divided by retail selling price

The cost of sales worked out is then deducted from Cost of Goods available for sales to determine the closing inventory/stock.

The schedule attached shows the relationship between cost and retail and how we arrived at a closing inventory of $294,932

Answer:

C. Mission

Explanation:

The Mission of a company states its reason to exist, what is does, how it provides or adds value to the markets, and what methods are used to produce the goods and/or services that the company offers.

The Mission is very important for a company because it is the general guideline that leads the organization in its daily operations. This is why the responsability of carrying out the mission falls under the CEO, the maximum administrative authority in a firm.

Answer:

c. depends on a number of factors, and can vary from one manager, location and type of employees.

Explanation:

A manager can be defined as an individual who is saddled with the responsibility of supervising and ensuring his subordinates (employees) are working effectively and efficiently with the organization's goals and objectives.

In Business management or human resource management, span of control can be defined as the number of subordinates or junior level staffs who are directly controlled by a superior (manager).

Basically, the span of control for a manager depends on a number of factors, and can vary from one manager, location and type of employees.

<em>This ultimately implies that, span of control is directly proportional to the organizational structure and any other factor around them.</em>

The master promissory note is a document that explains your rights and responsibilities as a federal student loan borrower.

The first option is correct. This document is one that is legally binding. Before a student agrees that they would want to take out loans as students, they first have to know what their rights and responsibilities are as a borrower and also to the lending facility.

There are a lot of available options that are in place to help with the management of student loans.

Read more on brainly.com/question/25038347?referrer=searchResults