Answer:

HPR = 0.371%

Explanation:

we must first determine the price of the bond in 1 year:

present value of face value = $1,000 / (1 + 6.25%)⁶ = $695.07

present value of coupon payments = $52.50 x 4.87894 (PV annuity factor, 6.25%, 6 periods) = $256.14

market price in 1 year = $951.21

since you bought the bond at face value (market value = YTM), the the holding period return is:

HPR = [(ending price - actual price) + dividends received] / actual price

HPR = [($951.21 - $1,000) + $52.50] / $1,000 = $3.71 / $1,000 = 0.371%

Answer:

$8.6

Explanation:

Calculation for How much total interest is he charging

First step is to calculate the present value (PV) using financial calculator by using this formula

PV=PV(Rate,Nper,PMT,FV,Type)

Rate represent Interest Rate

Nper represent Period

PMT represent Payment

FV represent Future Value

Type = 1 which represent the annuity due reason been that the 1st payment is to be made today

Let plug in the formula

Rate = 2%

Nper = 6

PMT = $30

FV = 0

Type = 1

Hence,

PV = PV(2%,6,30,0,1)

PV= $171.40

Since we have known the PV the last step is to calculate the total interest

Using this formula

Total interest =( PMT*Nper)-PV

Let plug in the formula

Total interest = ($30*6) - $171.40

Total interest = $180 - $171.40

Total interest = $8.6

Therefore the amount of the total interest he will be charging is $8.6

The minimum price that this order could be offered is at cost. Since there are no cost figures in this question, this is the best answer I can give.

You would need to at least sell the item for the amount of money it cost you to make, assemble, and ship the product.

Answer:

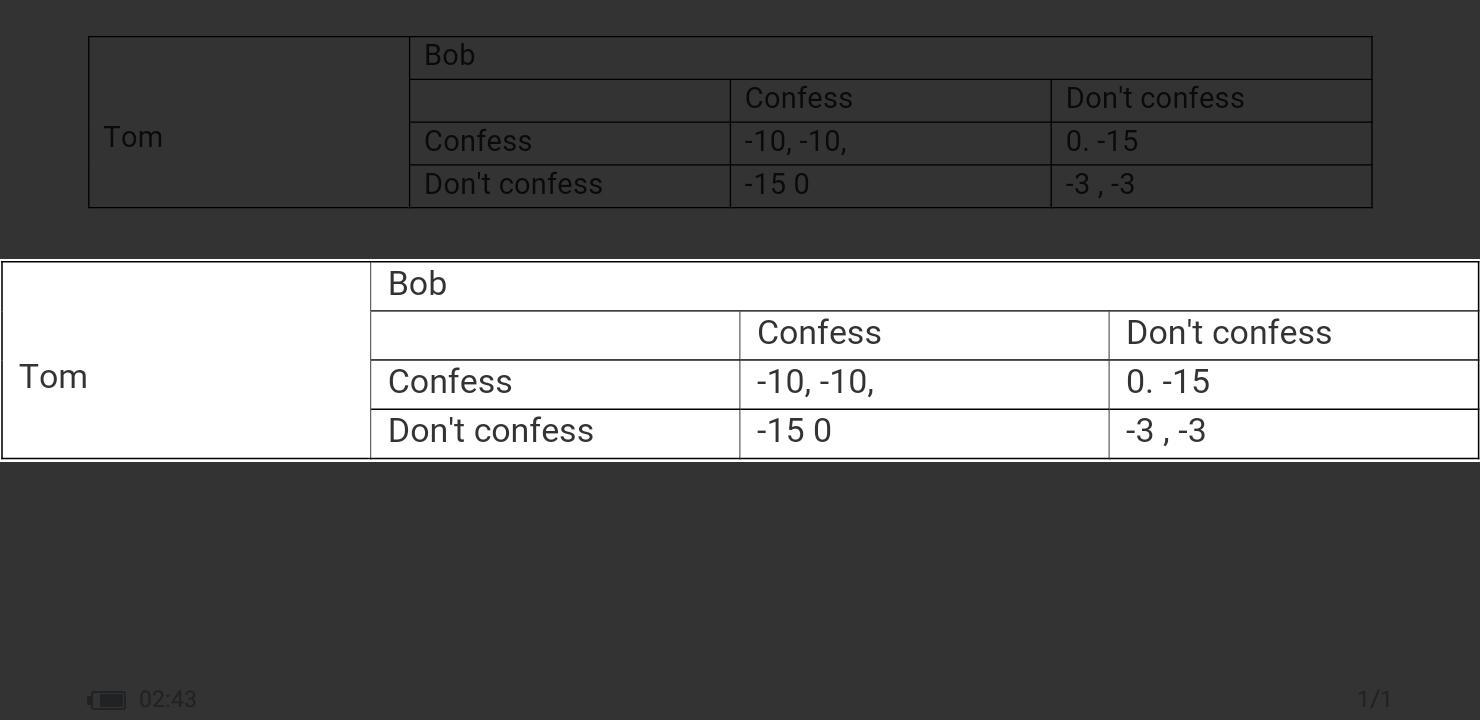

A. Check the attached image for the payoff matrix

B. Confess

C. Confess

D. 3 years. They could have avoided this by confessing.

Explanation:

The above question is known as the prisoner's dilemma. It is a form of game theory. It analyses the best option for a player in a game without regard for what the other player does.

The dominant strategy is the best decision for the player without considering what the other player does or without cooperation between the players. The dominant strategy for each of the prisoners is to confess because if one confesses and the other doesn't, the one that confesses goes free. If both prisoners confesses, they get 10 years each. These is a better option than not confessing and getting either 3 years or 15 years of prison sentence.

Because both players don't confess, hence they get 3 years in prison. They could have avoided the sentence by confessing.

I hope my answer helps you

<span>There are four methods in order for Martha to sell her product to prospective buyers:

</span>1. Know the principal attributes of a product.

<span>2. Find how the customers rate are choosing these with respect to these attributes.

</span><span>3. Find where the company's product is on these attributes in the customers mind

</span><span>4. Place the company in a different poition in the minds of the customers.</span>