Dupli-Pro Copy Shop provides photocopying service. Next year, Dupli-Pro estimates it will copy 2,800,000 pages at a price of $0.08 each in the coming year. Product costs include: Direct Materials, Direct Labor, Variable Overhead and Total Fixed Overhead.

How are additional product costs specified?

Product costs are often referred to as "inventory costs" or "manufacturing costs." Permanent costs: - Selling and administrative costs. These costs are reflected in the income statement as incurred.

Is the product costs advertised?

Sales commissions, administration fees, advertising and marketing, and office space rentals are all recurring fees. These charges are not covered as part of the cost of purchased or synthetic items, but are recognized as charges in the profit and loss account for the period in which they are incurred.

Is the rental the product costs?

When a manufacturer leases its manufacturing equipment and systems, the lease is the product costs (rather than the price of length). In other words, the rent is protected against the manufacturing overheads assigned to the manufactured product.

Learn more about product cost here:- brainly.com/question/24494976

#SPJ4

Answer:The product margin for product M5 is $7,385

Explanation:

To calculate the product margin for product M5,

Processing 3,870 ÷ 9,000

= 0.43 per MH

Supervising 25,000 ÷ 1,000

= $25 per batch

To calculate the overhead cost for product M5

Processing 0.43 per MH × 500

= $215

Supervising $25 per batch × 500 batches

= $12,500

Total = $12,500 + $215

= $12,715

To calculate the product margin for product M5 under activity based costing

$

Sales. 95,400

Less:

Direct materials 32,500

Direct Labour 42,800

----------------

Prime Cost. 75,300

Add: Overhead 12,715

----------------

Total Cost of production. 88,015

-----------------

Product Margin. 7,385

------------------

You should contact the company and tell them that you saw this and let them deal with it

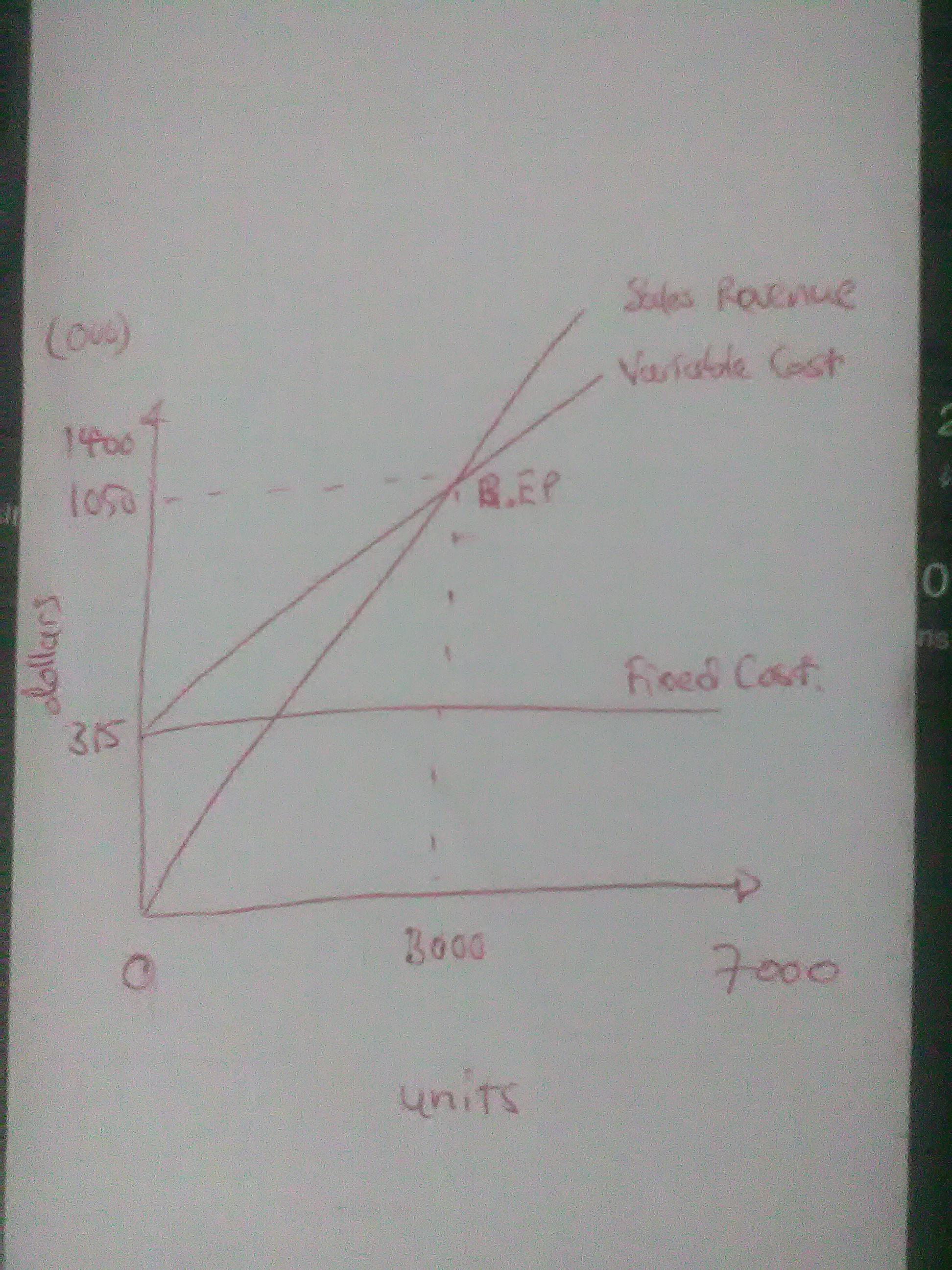

Answer:

1a. 3,000 units

1b. $1,050,000

2. See attachment.

3. contribution margin income statement

Sales ($350 × 7,000 units) $2,450,000

Less Variable Cost ($245 × 7,000 units)) ($1,715,000)

Contribution $735,000

Less Fixed Costs ( $315,000)

Operating Profit $420,000

Explanation:

Break-even point (sales units ) = Fixed Cost ÷ Contribution per unit

= $315,000 ÷ ($350 - $245)

= 3,000

Break-even point (sales dollars) = Fixed Cost ÷ Contribution Margin Ratio

= $315,000 ÷ ($105/$350)

= $1,050,000