Please find attached the graphs containing the requested information

The dominant cause of the increase in the price of hamburgers can be determined by the direction of change on quantity demanded: If the equilibrium quantity of hamburgers decreases, then the supply shift in the market for hamburgers must have been larger than the demand shift.

The demand curve shows the relationship between price and quantity demanded. The demand curve is negatively sloped.

The supply curve shows the relationship between price and quantity supplied. The supply curve is positively sloped.

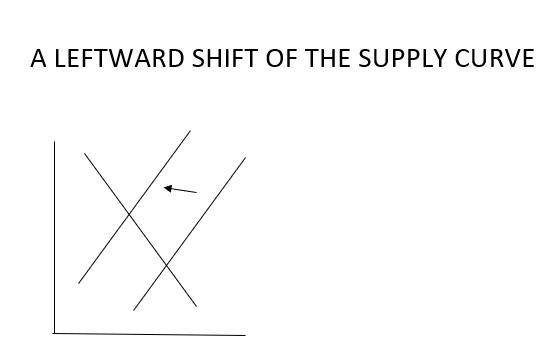

<u>If the increase in the price of</u><u> hamburgers</u><u> is as a result of </u><u>burger joints </u><u>closing down. </u>

If burger joints closes down, the supply of hamburgers would decrease. The supply curve would shift to the left. As a result of the leftward shift of the supply curve, equilibrium price would rise and equilibrium quantity would decrease.

<u>The increase in the price of </u><u>hamburgers</u><u> is as a result of a decrease in the price of </u><u>French fries.</u>

Hamburgers and French fries are complement goods. Complement goods are goods that are consumed together. An decrease in the price of French fries would lead to an increase in the demand for hamburgers. This would lead to a rightward shift of the demand curve while the supply curve remains unchanged. As a result, both equilibrium price and quantity would increase.

If both events are partially responsible, the supply curve would shift to the left, leading to an increase in price and a decrease in quantity and the rightward shift of the demand curve would lead to an increase in equilibrium price and quantity.

If the decrease in supply is the dominant factor, there would be a decrease in equilibrium quantity.

If the increase in demand is the dominant factor, there would be an increase in equilibrium quantity.

To learn more about demand, please check: brainly.com/question/14456267?referrer=searchResults